A Fund Manager’s Guide to Bonds

OIJ #47 | Everything you need to know in one post. Gov/Corporate Credit, Hidden Spreads, and the Art of Not Holding the Bag

This week, we are diving into a bit of a masterclass on a topic I think is absolutely crucial to understand. Consider this the first of a two-part series.

I actually prepped these posts in anticipation of my new interns arriving next week, partly to train them, and partly to make sure they don’t break anything on day one. These two topics are the core fundamentals that explain pretty much everything I do.

This first post will cover debt and how to evaluate bonds.

The second will dive into due diligence.

Specifically, how to conduct a thorough, deep-dive forensic investigation of a business.

To keep things practical, I’ll be using simplified examples of actual deals I’ve analyzed and real due diligence I’ve conducted in the past (as well as live transactions I’m working on right now).

If you want to join our community of investors, this is your chance:

It’s free.

Fascinatingly, surviving both bonds and acquisitions usually comes down to mastering a single, definitive document.

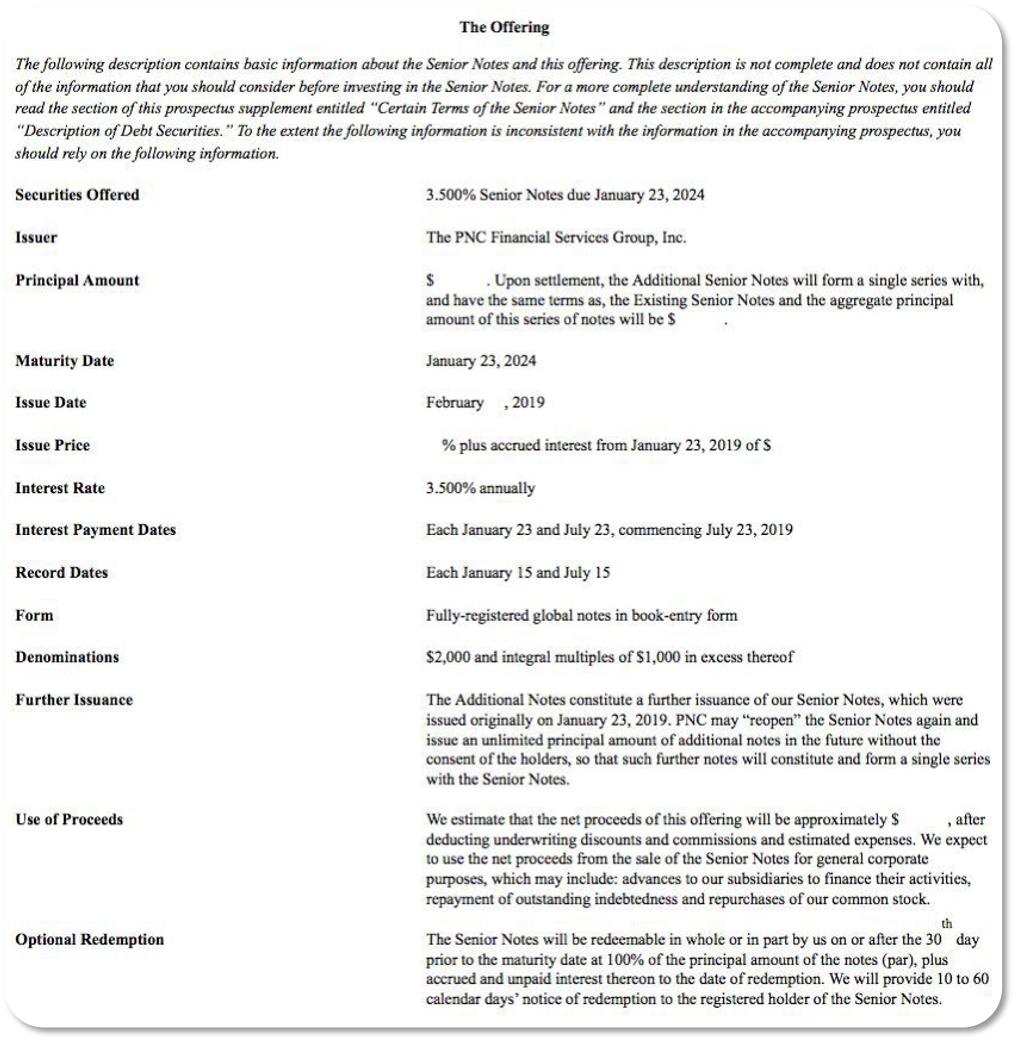

For bonds, that document is the prospectus. The bond prospectus essentially outlines the covenants, the legally applicable rules of the game.

These are usually massive, soul-crushing mountains of legalese that no sane person wants to read. But if you’re putting real money to work, you absolutely must read them.

Why?

Because buried in that fine print is every single way the issuer can legally screw you over. You want to be very, very aware of what’s hiding in those pages.

When it comes to due diligence on an acquisition, the holy grail document is the Share Purchase Agreement (the SPA).

The SPA is where deals go to live or die. No matter how brilliant your due diligence is, there will always be missing pieces or weird day-to-day operational quirks that you won’t truly grasp until you actually own the keys to the kingdom.

Therefore, drafting the legal conditions to handle those unexpected ‘unknown unknowns’ is the most critical part of the entire process. It’s a two-front war: not only are you studying the business meticulously so the “worst-case scenario” stays as small as humanly possible, but you are also using the contract to build a fortress for when the unexpected inevitably happens.

My name is Bondo, Jamesu Bondo

So going back to this post: bonds, bonds, bonds, bonds, bonds, bonds, bonds, bonds, bonds, bonds, bonds, bonds, bonds, bonds, bonds...

Can’t live with them, can’t live with them.

Bonds sort of explain the returns on everything we see in the financial markets.

On the one hand, highly popularized equities are sort of in vogue right now. But back in the day, say until the 50s or 60s, bonds were essentially everything that was transacted. Back then, everything else was considered way too risky to invest in.

That is, until a guy called Michael Milken, came over and unlocked the lower tiered bonds and essentially equities. He ended up cheating though, so he’s probably not the example of how to invest.

With that in mind, the same basic concept, applicable to bonds, applies to modern instruments. So once you understand it, you pretty much understand investing.

Debt. Feeding the Capitalist Machine

Bonds are the stable bedrock of the financial system. If the world has, let’s say, $100 trillion worth of equities (probably way more than that), you probably have 3-5 times that amount in debt for those same companies plus asset-backed private debt and non-backed business debt (not to mention derivatives). Think about everything including mortgages, bank loans for small businesses… stuff like that.

Debt is what helps everything run smoothly and, to be honest, accelerates projects. It makes things possible for people. You can think of it as the ultimate form of crowd-sourcing of resources.

Even when a venture capital fund comes over and backs a startup, that money is usually not equity at first, it often comes in the form of convertible debt. So that flexibility is exactly how things get started.

Same thing goes for buying a house. People don’t usually have a million bucks just sitting around. But if you have 20-ish% of that amount, you can lock down the house and finance the rest. The whole point is that you get the asset and you get the ball rolling. In essence, debt is the rocket fuel for capitalism. And in that sense, it’s great.

But obviously, there is a dark side. Taking out a loan to purchase a depreciating asset or a consumable is a terrible choice. The brutal thing about debt is compounding interest. It compounds beautifully for the person lending to you, but if you’re the borrower, it compounds against you… effectively cannibalizing your future cash flows.

So depending on what you’re using it for, debt is technically ‘good’ or ‘bad’.

The same applies to the terms of the debt.

I’m sure you’ve seen people get trapped by bridge loans, or what we call Cofidis style predatory loans in Spain. Those small-time lenders will gladly hand you cash, but they’ll charge you a 30% annualized interest rate for the privilege. Same goes for credit cards charging 20% to 30%.

Taking these out is financially indefensible. Sure, people use them out of necessity, but the hurdle rate to pay them back is just insane.

Interest compounds!

NEVER FORGET THAT.

It’s one of those silent killers that will destroy you as an individual, and even faster as a corporation. By definition, that is really, really, really bad debt.

Mechanics of a Bond

Now, let’s look at the actual mechanics of institutional debt. Here, we live at the intersection of cash flows, predictability, and risk management.

When you buy a stock, you’re basically praying that the company grows, margins expand, and the market rewards them (via multiple expansion). A bond is a much more calculated, cold-blooded move. It’s essentially a hard legal contract. You are handing over capital, and that capital must be paid back to you at a specific rate, at a specific point in time, with a specific interest.

You’re going to have four major components to debt that you must understand.

Deconstructing this, first you’re going to have the (#1) face value. The face value is just the amount you lent out (also called the principal amount), and usually, bonds are issued in blocks of a thousand bucks ($1,000 per bond).

Then you have the (#2) coupon rate. The coupon rate is just the interest percentage of that face value that the issuer pays you every year.

Note: As the secondary market price of the bond changes, that fixed coupon plus alternations in price will give you a different yield. Who is giving out the bond matters immensely here.

We’ll talk more about this in the future, but it’s not the same to hold Uncle Sam’s debt as it is to hold debt for a municipal highway. Nor is it the same to hold debt from a speculative micro-cap company versus a massive blue-chip giant like Google. Corporate bonds are definitely not created equal.

But the unique thing about bonds is that they have a strict issuance date and a (#3) maturity date. Maturity is when you get your principal payment back, and issuance is just when that money first goes out.

Because that’s the case, whatever happens to market interest rates in the meantime heavily affects the trading price of these bonds.

This is because, once in the secondary market, bond prices are completely relative.

If the Fed chairman decides that interest rates go up, any newly issued bond will have to pay a higher interest rate to attract investors. In relative terms, already existing bonds with lower coupons will immediately be valued at less money, because you’re holding a worse deal compared to the new bonds hitting the market.

With that in mind, do remember that the face value is a constant at the point of issuance and at the point of maturity. If you lent out a million bucks in blocks of a thousand, that exact money has to be given back to you at or before the end of the period. Whatever happens in between is just a product of interest rate fluctuations and market moves (speculation).

The initial value and the end value are the same. But in the meantime, you can buy or sell that bond at a discount or a premium.

A discount is when the bond sells below face value (say, $900), and a premium is when it sells above face value (say, $1,100).

Again, going back to the fundamentals, that coupon rate is fixed. If a bond is put out at 5%, it’s going to give you that fixed $50 a year over a $1,000 face value. But that fixed $50 keeps getting divided by a different market price every single day between issuance and maturity, and that math gives you your current (#4) Yield to Maturity (YTM) or yield for short.

Yield is something we talk a lot about, particularly for government bonds. It’s a shifting factor that accounts for the difference between the face value and the current market price. Let’s say a bond was issued at $1,000 and is now priced at $900. That $100 discount, combined with the regular coupon payments, will give you what is known as the yield.

Note: Let’s look at the quick math. If this 5% coupon bond has 3 years left and trades at $900, your total return comes from two places:

You get $50 in cash every year.

You make a $100 capital gain at maturity ($1,000 face value minus the $900 you paid). Spread over 3 years, that adds roughly $33.33 of extra value per year.

Add those up, and your average annual return is $83.33. Divide that by the average value of the trade, essentially initial and final value, ([$1000 + $900)] /2 = $950), and you get a back-of-the-envelope yield of 8.77%.

(The mathematically exact YTM using a spreadsheet is 8.92%, meaning this quick shortcut gets you within striking distance in under five seconds)

YTM is the total return of the bond, combining both capital gains (or losses) and the coupon rate paid in the meantime. When institutional fund managers talk about yield, this is exactly what they’re discussing. This is the gold standard for valuing a bond or, more importantly, understanding its true value.

Just like we use 15% FCF as a barrier for entry, you can apply the same logic here to determine a minimum hurdle.

Risky Business

Risks on these? There are obviously a few additional nuances, but I’d say the two primary risks are duration risk and default risk.

Duration risk is also known as interest rate risk. It simply measures how sensitive a bond’s price is to changes in interest rates. Even though this duration risk is technically a temporary, paper-driven thing (until you sell the bond, everything is just an unrealized gain/loss), it can completely wreck institutional balance sheets.

Take banks, for example.

Banks have a lot of debt on their books, and duration mismatching is one of their biggest hazards. If a bank’s depositors need their money back in two years, but the bank invested that cash in 10-year bonds, they have a massive mismatch.

If interest rates spike upwards in the meantime, those 10-year bonds become far less valuable. If the bank is forced to liquidate them early to meet depositor withdrawals, they realize those massive losses, cratering the equity value of the bank. This creates a vicious spinning wheel, exactly like we saw back in 2023 when regional banks collapsed due to a mismatch of what timeline they should own versus what they actually own.

Again, if you hold a bond all the way until maturity, duration risk effectively drops to zero. So it really depends on what your balance sheet looks like. If you only buy bonds with cash and you don’t use leverage, duration risk is essentially a non-issue because you are just going to hold the asset and collect your principal back at the end of the contract.

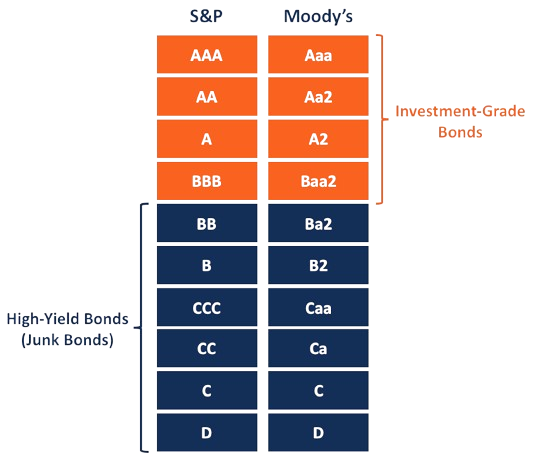

The second risk is default risk, and this one is a threat to everyone. It’s also known as credit risk. This is technically monitored and graded by the big rating agencies. I’m sure you’ve heard of S&P, Moody’s, and Fitch. They operate as a natural oligopoly. The government handed out a ton of licenses back in the day, but the market naturally concentrated around these three major players.

What they created is a standardized trust scale for what is ‘good’ debt and what is ‘bad’. The two major categories are Investment Grade and High Yield (also known as junk bonds).

Anything rated BB+ or below is technically considered high yield. Everything above that (from BBB- all the way up to a flawless AAA) is considered investment grade.

For context on these ratings, the US Government sits at the top tier (around AA+ or AAA depending on the agency), while a small, highly leveraged micro-cap company will probably sit deep in the junk bond category.

Think of something like Aurora’s debt. According to the market, these smaller companies don’t have the immediate ability to guarantee repayment or control the macro environment around their debt. Therefore, you’re dealing with two completely different worlds of risk.

Credit or default risk refers strictly to the permanent loss of capital.

In the case of a major government, they can print their own currency, so it is technically impossible for them to default on nominal terms. You still face inflation risk (since printing money devalues its purchasing power), but the default risk itself is pretty much non-existent.

The exact opposite applies to a small company. They don’t have a printing press. You’re getting a much higher interest payment (higher yield) just to hold their debt, but if they hit a wall because of an imbalance in their assets versus liabilities, you’re the one holding the bag.

As bondholders, our upside is hard-capped. The maximum return we can ever get is our coupon plus our money back. Because our upside is limited, if the company goes under and can’t repay, you are going to get pennies on the dollar in bankruptcy court, and there isn’t much else you can do about it.

Curving the Yield

Lastly on this part, you have the concept of the yield curve. The yield curve is sort of... how should I explain this? Well, it maps out the difference in time, and time in this case really conditions risk.

Generally speaking, the longer the lifespan of a bond, meaning the more time between when it’s issued and when you get your principal back, the riskier it is.

Because of that, you’re usually going to see an upward slope, which we call a normal yield curve. The curve goes upwards because as you transition from, say, a 10-year to a 30-year debt instrument, you demand a higher interest payment to lock up your cash.

The future is unpredictable, and you face two major risks over long periods: inflation eating away at the purchasing power of your principal, and general macro uncertainty. More uncertainty means you demand a higher premium.

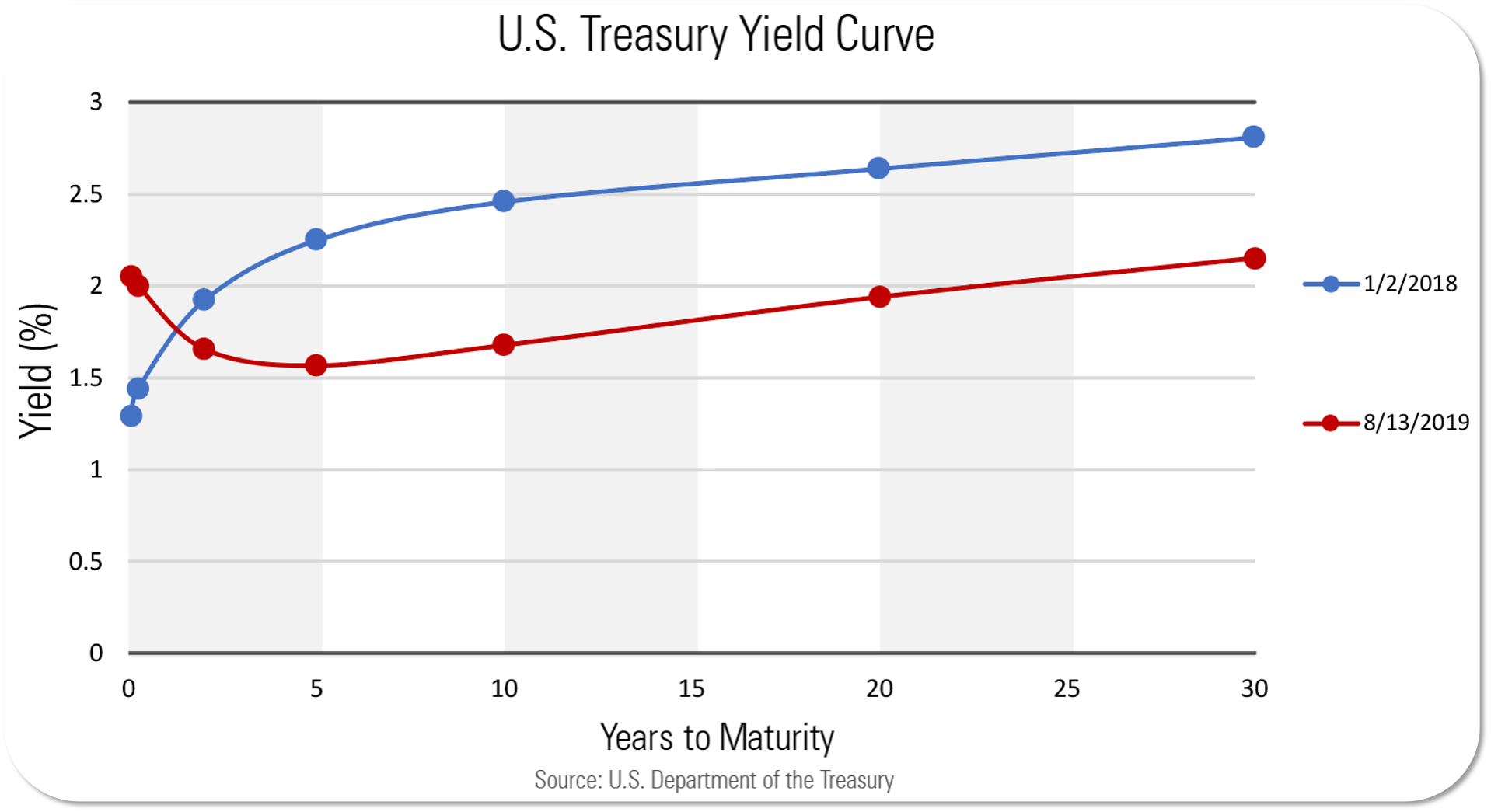

However, this curve can invert.

Sometimes, the yield on short-term debt becomes higher than long-term debt just because immediate, near-term uncertainty is extraordinarily high. An inverted curve is usually a stellar leading indicator of an incoming recession.

These inversions are heavily driven by supply and demand dynamics, often influenced by central banks. For example, when a central bank adjusts interest rates or a foreign central bank aggressively buys or sells short-term paper, that massive shift in demand heavily impacts the front end of the curve, the six-month to 24-month section.

These short-term outbursts of confidence (or panic) shake up the short end, while the long-term end stays relatively grounded in long-term economic growth expectations.

When that short-term rate spikes rapidly, it creates a very weird, upside-down situation where issuers are forced to pay more to borrow money for a few months than they are for 10 or 30 years.

Printing Presses vs. Productive Assets

Going deeper into credit itself, there are two major flavors: government bonds and corporate bonds. We just talked about the general trade-offs between the two, but understanding how they interact is really where you build your ability to specialize.

Note: For example, my specific edge lies in navigating niches like oil and gas corporate bonds, specifically on the junior mining, exploration, and tech-driven mapping side of the sector.

Different industries and issuers obviously command different interest rates, and that gap is dictated by what is known as a credit spread. The credit spread is a foundational concept you need to master; think of it as the risk-premium layer stacked on top of baseline interest rates.

To map this out, major government bonds (like US Treasuries) are typically treated as the ‘risk-free’ rate, which serves as the global benchmark for valuation.

Note: If you want to check out exactly where you country lies, in the industry we all use the Damodaran Resource. It’s the most accurate way of getting a pinpoint figure for discount rates.

However, once you look outside of rock-solid economies, you introduce country risk.

Take a country like Argentina, for example. If you want to price debt there, you start with the baseline risk-free rate, and then you have to tack on a plus, essentially an additional yield premium that international investors demand just to take on the geopolitical and macroeconomic risk of investing in that specific country.

Right now, that country risk premium for Argentina hovers around 5% (500 basis points) as they attempt market normalization, though historically it has spiked as high as 25% during major crises.

How does this impacts corporate bonds?

If you are analyzing a corporate bond issued by a private company operating inside Argentina, an investor is going to demand a stacked combination of yields.

Your total interest rate is going to equal:

Total Demanded Yield =

Risk-Free Rate + Country Risk Premium + Corporate Credit Spread

So in practical terms, if the global risk-free rate is 4.5%, the Argentine country risk premium is 5%, and the specific operational risks of that oil exploration company require another 5% spread, the final interest rate on that corporate bond will be at least 14.5%.

Obviously, there are additional technicalities like liquidity and structural covenants that play into this (essentially making people demand higher rates), but that is the exact core architecture of how credit is priced globally.

Death and Taxes

Another core pillar to understand is the taxation on these bonds.

Just like any other financial instrument, when you make money, the taxman wants his cut. However, to incentivize investments within public works, a lot of municipal bonds (debt issued by local cities or states) are completely tax-free.

You absolutely should factor this into your math; sometimes, investing in a muni bond can be extra juicy because that tax exemption significantly boosts your net, after-tax yield compared to a fully taxable alternative.

This ties directly into the actual purpose behind issuing the debt.

There is a world of difference between a government raising money for public infrastructure, social programs, military spending, or just covering national deficits, versus a corporation raising money to build new factories, fund Research & Development, acquire competitors, or buy back their own stock.

(Or, in the case of a few tech companies nowadays, issuing corporate debt specifically to stack Bitcoin on their balance sheet).

In this regard, to be honest, government bonds are inherently lacking because most sovereign spending is non-productive in the strict capitalistic sense.

If you build a manufacturing plant with corporate debt, that factory produces a product, generates sales, and automatically becomes a cash-generating asset.

That is exactly how debt should be used, in my opinion.

When you borrow money to fund non-productive spending, you are adding structural risk to the system. At the end of the day, you need tangible cash flows to service and pay back debt. If you invest the borrowed principal into an asset that naturally multiplies cash flows, paying back the lender becomes a highly predictable outcome. If you don’t, things get complicated.

Liquidity

(I was going to use the official Liquidity Summit logo here, but I don’t want the All-In guys suing me. I can’t afford Chamath’s lawyers, and quite frankly, my incoming interns aren’t qualified to handle a deposition yet)

And I’d say the final major difference between these two worlds is liquidity.

A lot of those high-yield, wide-spread corporate bonds are incredibly illiquid. If you try to buy or sell a massive block of them, your transaction alone can drastically move the market price against you.

That is definitely not the case for major government bonds, purely given the staggering size of the sovereign market. It is virtually impossible to dump a few hundred million bucks of US Treasuries and noticeably affect the global price.

However, corporate credit is a completely different story, especially on the private debt side of things that has exploded in popularity recently.

In private credit, you don’t hold publicly traded papers; those bonds are entirely private. When you want to exit your position, you can’t just press a button and dump them into a public exchange. You have to find a specific buyer and negotiate the entire transaction on a one-to-one basis.

This introduces heavy counterparty friction and severe liquidity constraints. If you ever find yourself in a position where you need your money back fast, that structural illiquidity can be a total recipe for disaster. And I mean global disaster given the size of this market.

Bond Valuation

Bonds are beautifully straightforward. In my opinion, the way you value a bond is the exact same way you value an equity… it’s just that bonds have a massive layer of certainty baked into them.

At its core, it’s just a DCF (Discounted Cash Flow) model. You are simply summing up all the projected cash flows from right now until judgment day.

When you value a stock, you have to project a terminal value out to infinity because companies are theoretically designed to run forever. But with a standard bond, you don’t need to guess about infinity. There is a hardcoded beginning and an end. Unless you are dealing with perpetual bonds (which we’ll talk about in a second), you know exactly when the contract terminates, and that total return is beautifully captured in the yield.

To do the math on a bond DCF, you just take each scheduled cash flow and divide it by (1 + r)^t, where r is your required rate of return (effectively the yield).

This discount rate acts just like the WACC (Weighted Average Cost of Capital) you use in a regular corporate DCF. When you add all these discounted slices together, you get the fair intrinsic value of the bond.

Again, it’s exactly like evaluating a business, but your coupon payments are legally contracted. You know exactly how much they are supposed to pay you and when.

In my opinion, this concept should be literally branded into your brain because mastering bond mechanics is the absolute best way to truly understand how DCFs work and how to value any asset.

Without predictable cash flows, you aren’t really investing… you’re just speculating.

Apply this exact logic to the market, and the line between a calculated play and a blind bet becomes crystal clear:

Gold vs. a Gold Mine: A brick of gold sits in a vault, generates zero income, and costs you storage fees. That’s speculation. You’re just praying someone buys it for more later. A gold mine is an investment; it extracts a commodity, sells it, and throws off actual free cash flow.

A House: Buying a property just hoping the neighborhood appreciation skyrockets is speculation. Buying a rental property that collects a predictable, monthly cash check from a tenant is an investment.

Cryptocurrencies: And, of course, the ultimate modern speculation. Crypto has no earnings, no coupons, and no cash flows to discount. Your entire thesis relies on the Greater Fool Theory, pretty much the hope that someone else will pay more for your digital tokens tomorrow (including supply/demand dynamics).

The fundamental difference between a bond and every other cash-generating asset on earth is simply the contractual certainty of its cash flows. And that certainty, of course, always commands a premium.

Getting Paid Today

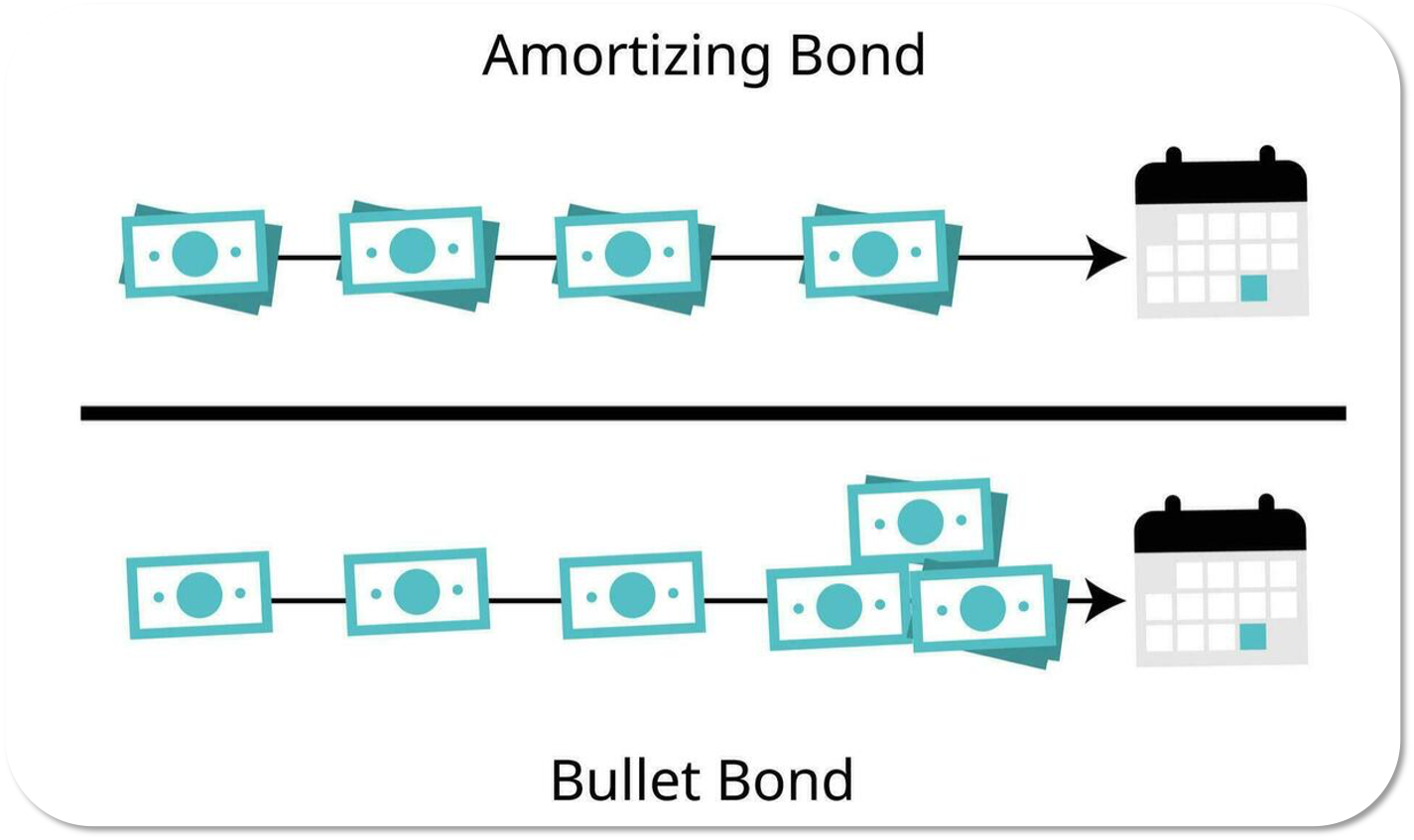

As for return structures, the absolute classic is what we call a bullet bond.

With a bullet structure, you invest your capital on day one, you collect regular interest payments along the way, and then the issuer hits you with a single, massive bullet payment of your entire principal at the very end.

But that’s not the only way debt is structured. You also have amortizing bonds.

You can think of these exactly like a home mortgage. With every single payment, the issuer pays you back a mix of interest and a piece of the underlying principal.

By paying back the principal gradually, they are constantly reducing the total amount of money they owe you, which naturally decreases the size of the interest payments over time. You see this layout all the time in real estate mortgages, certain corporate bonds, and specifically in government debt when the market doesn’t fully trust the country.

Argentina, for example, has some very famous restructurings where they issued bonds denominated in USD. Because the market was highly skeptical of lending to them long-term, Argentina had to issue amortizing bonds.

This structure systematically reduces the counterparty risk (government defaulting at maturity) by forcing them to pay back chunks of the principal early. For a country that has defaulted on its debt multiple times throughout history, investors demand those kinds of hard assurances.

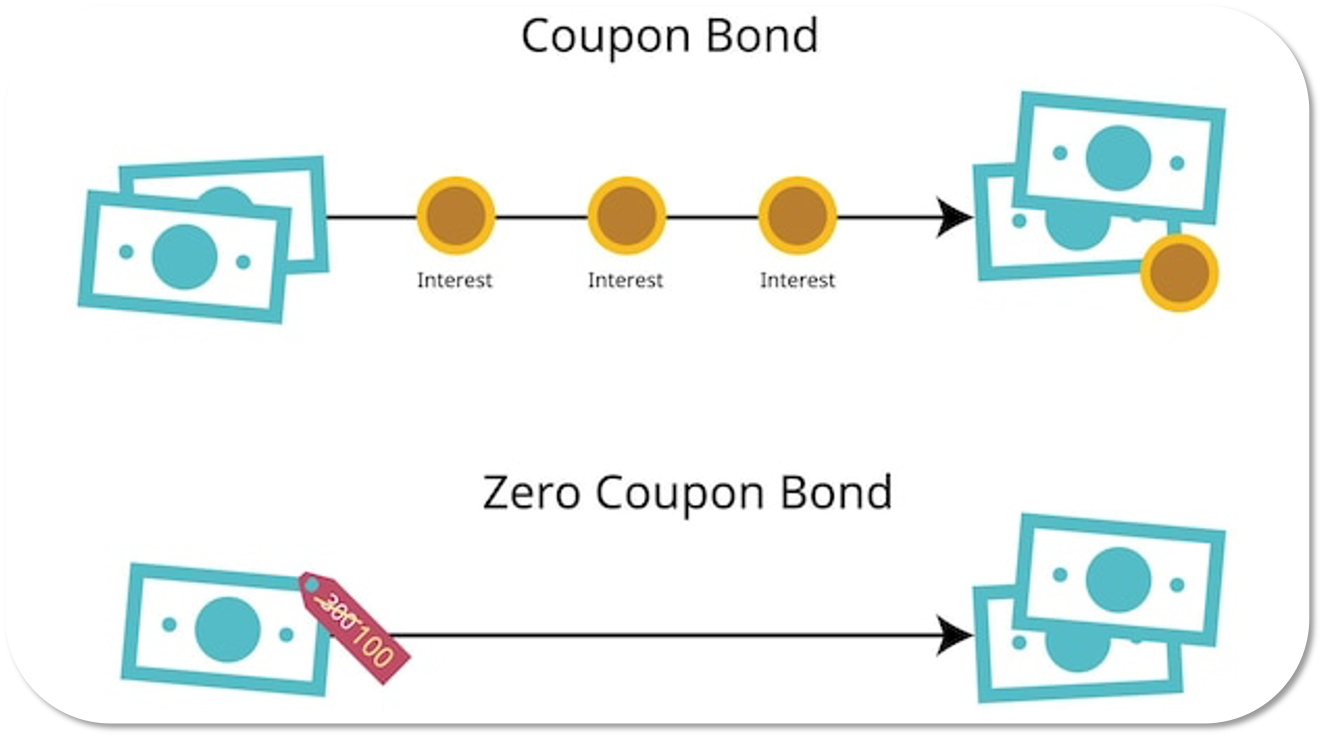

Another major variation is the zero-coupon bond. These bonds have absolutely no ongoing cash flows, they completely strip out the coupon side of things.

Instead, they are issued at a deep discount. So instead of buying the bond at a face value of $1,000 like a standard issue, you might buy it today for $600 or $700, with the binding promise that the issuer will repay you the full $1,000 par value at maturity.

Because you don’t receive any intermittent payments, zero-coupon bonds carry extreme duration risk. They are hyper-sensitive to interest rate fluctuations. Any slight shift in the market discount rate will violently swing the value of a zero-coupon bond, because your entire return is back-loaded onto the very last day.

These instruments are incredible tools if you are macro-trading a high-interest-rate environment where you expect rates to plummet, or if you are investing in a hyper-stable environment where you want to lock in a return without the operational hassle of managing monthly cash distributions.

The final category is perpetual bonds. These are bonds with absolutely no maturity date. They promise to pay you a fixed coupon from now until judgment day, but they never have to give you your principal back.

In my opinion, most historical perpetual bonds have been massive scams, think of old wartime bonds and the like.

Perpetual bonds suffer from a fatal flaw: over long periods, governments will inevitably print a mountain of money, inflating away the real purchasing power of that fixed coupon payment.

Unless you are buying an antique certificate to frame and hang on your office wall as a cool collector’s token, perpetual bonds have historically been a terrible place to store wealth across the centuries.

The Art of Living Off Contractual Cash Flows

To sort of wrap these things up, the total return for an investor in the bond market comes from three distinct elements.

First, and most obviously, you have the coupon payments. These are the regular interest payments sent over to you. Nothing changes here unless the bond completely defaults; they are rock-solid cash streams.

The second way you make money is through capital gains (or losses), which is simply the difference between the face value and whatever price you actually paid for the bond. If you purchase a bond on the secondary market at a discount, meaning you pay less than par, and you hold it all the way to maturity, the issuer must pay you back the full par value. That price convergence hands you a nice capital gain.

Now, it’s highly unlikely that this capital gain will be massive under normal circumstances because bond upside is strictly capped. Trying to chase explosive, stock-like returns in the bond market is incredibly risky.

If you are buying a distressed bond trading at, say, 20% of its par value, the market is screaming at you that the company is on the verge of bankruptcy. If they somehow survive and pay you back, sure, you make a spectacular 5x return. But chances are you will likely never see your money again.

I wouldn’t say those distressed bonds are completely worthless, but they are highly complex corporate turnarounds that you don’t want to mess with unless you are a specialized distressed-debt investor.

The final element, and one most people discard, is the reinvestment of your income.

The unique thing about bonds is that they are constantly throwing off cash, especially if you hold an amortizing structure. Because you are getting your liquidity back early and often, what you choose to do with that incoming capital is completely up to you.

Let’s do the math: if you buy a million-dollar bond paying a 10% interest rate, you are collecting $100,000 every single year. In the bond market, interest is typically paid out semi-annually. So every six months, a $50,000 cash chunk hits your account.

Unlike equities, where you often deploy a million bucks into a stock and have to wait years until you liquidate the position to realize a return, bonds unlock recurring liquidity. Unless a stock pays a high dividend, you rarely see that kind of consistent cash flow.

What you do with that $50,000 every six months is entirely up to you. But if you roll it over and reinvest it into new income-generating assets, it creates a powerful secondary compounding effect. This reinvestment rate is truly the hidden engine of the fixed-income world.

I hope you enjoyed this masterclass, I hope the real-world examples were useful, and most importantly, I hope you learned a ton about how the global debt machinery moves.

I look forward to seeing you all in part 2 next Wednesday, where we will be doing a deep dive into forensic due diligence.

This is the absolute master key behind the investigative scuttlebutt research we do to find hidden gems in the market, and we’ll use a private company as an example (as it required an even more thorough examination).

See you then!

If you found value in this analysis, please hit the ❤️ button and share your thoughts in the comments. It helps us bring institutional-grade research to a wider audience.

And if you liked this post, we’re confident you’ll love this: