Welcome back my fellow Substack readers! I wanted to provide a quick recap of events that occurred in the last 6 months, including my thoughts and the mosaic of information at my disposal. Some of the key elements will remain private, but the following is a high-level commentary on my thoughts on Cardlytics. Please enjoy.

Note: I had already redacted the note by the time the latest events transpired. That being said, a few items came out yesterday regarding the settlement of the Bridg dispute which will lead to a $25 outflow for the company. The payment will be carried out in three payments with most of it ($20M) being paid in January 2024

The company trades at around the $315 M market cap mark including $90.0M in cash, and $66.8M to $74.8M in cash including variable legal contingencies. More information will be included below but I feel it’s important to note that both scenarios improve on the previous letter which assumed $60M in cash.

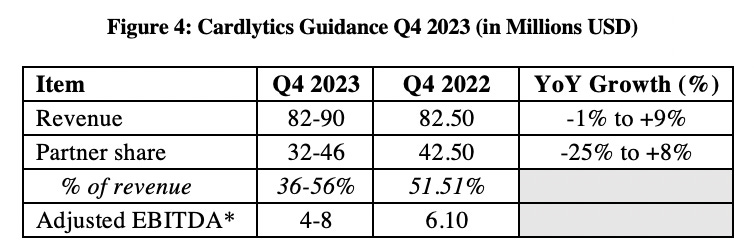

At the end of Q3, Cardlytics experienced high volatility to the upside. The company’s management used higher stock prices to make a few well-incentivized hires. However, the share dropped significantly once the company released earnings. The results are as follows:

Management also gave the following guidance for Q4:

*Cardlytics defines adjusted EBITDA as net loss before income taxes; interest expense, net; depreciation and amortization expense; stock-based compensation expense; foreign currency gain (loss); acquisition and integration cost (benefit); loss (gain) in fair value of contingent consideration; goodwill impairment and restructuring and reduction of force

I’m confident that after reading a few of these semi-annual updates you are shocked by the posting of earnings and guidance as part of the commentary. Be sure this is done with a purpose in mind. The following two tables serve to illustrate how the company has changed under new management.

Firstly, the company has noticeably sacrificed growth for profitability. Year-on-year growth estimates have slowed down to high single-digit or low double-digit figures. However, EBITDA and FCF have risen dramatically. This unpopular choice is a big win for shareholders as it prevents the two most feared outcomes i) dilution and ii) bankruptcy. With the latest changes to both the cost structure and the handling of bank partners (and their share of the pie), Cardlytics has ensured smooth sailing for the foreseeable future. This can be observed via the reduction in Partner share that was heavily affected by the contractual changes with JP Morgan’s (%) share. These changes occurred in late June, therefore their full effect will be manifested starting in Q4 2023.

The second observable change promoted by management is transparency. This was visible in the closer relationship between Cardlytics and bank partners via the integration of the cloud server, public statements from the banks, and the redefinition of metrics (mainly MAUs and ARPU). Cardlytics modified the transition to the AWS vocabulary from a certain 100% to a full transition. For the time being, JPM is the only major bank that has fully transitioned (US Bancorp is also on) which equates to 50% of users being on the server. This transition has resulted in a much higher level of both unique advertisers and offers. The legacy 45-day campaigns can now be modified mid-campaign to add or reduce the offer, and there have been multiple instances of campaigns with a shorter duration (down to 3 days).

New types of offer include:

- category level: only for certain items/categories within a store

- stackable: offer for a product and an advertiser can be selected simultaneously e.g. coffee $1 discount and Panera 10% discount can stack

- premium/membership: users already in a loyalty program get additional discount e.g. 10% off if no loyalty, 20% if member of loyalty program

- two-tier: 10% if <$20 spent, 20% if >$20 spent

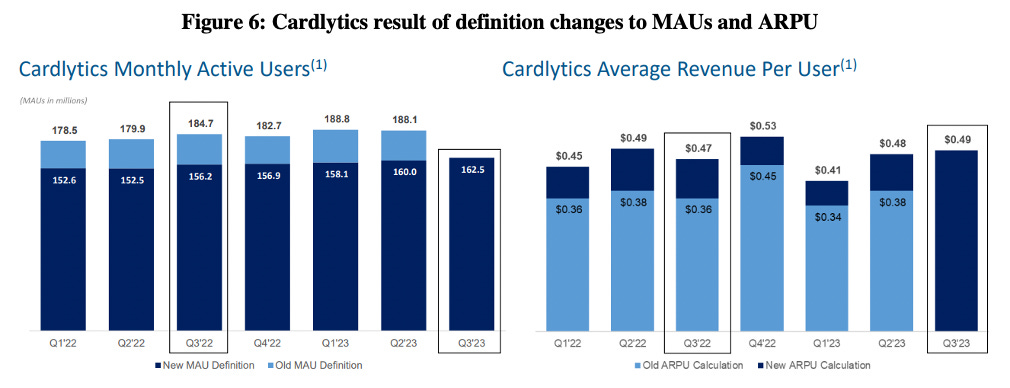

As more MAUs transition, one would expect to have both better offers and more types of offers. In fact, September closed with a $70 max and $18.44 average cashback (11% cashback), while December closed with a $200 max and $28.50 average cashback (10% cashback). With the transition, management can create and test as many offer constructs as they wish as permission will be dependent on a campaign level rather than a bank level. The following metrics show how Cardlytics has progressed in terms of advertisers. The figure should be partially correlated to revenues. Once again, as bank partners transition, the offering will be richer for advertisers which should result in higher demand for Cardlytics’s products.

On the metrics, Cardlytics (probably the new CFO) chose to redefine Monthly Active Users (MAUs) as singular cardholders when previously this metric stated the number of cards in use. This metric may not fully express unique cardholders as filtering within one bank can be easy, but filtering between banks may not. Nevertheless, the metric is a much closer proxy to the real number of active users that make use of Cardlytics’s services.

Note that these modifications do not change the total resulting from =MAUs * ARPU. The market’s sentiment changes towards extreme pessimism with this note perhaps out of the misunderstanding that Cardlytics had lost MAUs, or its equivalent, a bank partners. To me, the changes reflect positively on the new direction chosen by management.

News on cdlx, subsidiaries and competitors

Major bank partners took the stage from Q3 2023 onwards. JP Morgan used the migration to the new server and the renegotiations of terms to promote Cardlytics on a worldwide stage. For starters, Jamie Dimon mentioned the ads platform and restated their focus on commercial banking benefits during their quarterly call. The bank also blasted users with multiple email notifications and app banners funneling users towards specific offers powered by Cardlytics. Bank of America (BofA) changed course at the end of 2023 when it eliminated all non-Cardlytics offers on its platform. The bank is also showing strong signs of server migration as of January 2024.

Cardlytics renewed its interest in the UK by signing the neobank platform Monzo and its 8 million MAUs. In addition to multiple minor bank-related news, Lloyds Bank renewed its contract with Cardlytics extending the service until December 2026 and more likely than not conceding part of the bank share. There have been multiple accounts of rumors about the changes for bank share with other banks, but none have been confirmed.

LinkedIn has served as a powerful source of information as it provided 3 key clues that were later confirmed by news pieces and interviews.

i. The most noteworthy include an internal note stating a revenue goal of $350M for 2023. This message was posted multiple times on job postings across the platform.

ii. Philip McGahey, a former Cardlytics employee, linked the company with Mastercard’s loyalty program “SessionM” which would be similar to what Cardlytics probed in the past with American Express (Amex).

iii. Visa acquired a stake in cdlx.

This is quite a rare sight as the company has a four-stock portfolio with extremely low turnover. Visa purchased a small position that could have multiple implications for collaboration in the medium and long term.

There was an interesting development on the Bridg earnout. Cardlytics has not paid out the remainder of the settlement as the company appealed part of the results. The all-cash payment can range up to $23.2M, which was the expected outcome noted in previous letters. However, according to a few accounts, the number could be reduced to between $15M and $19M for the first earnout. The expected value of the second earnout remains at $0 as confirmed by the arbiter in May 2023.

On the product and subsidiary front Cardlytics launched in August a new data and media network product under the brand Rippl. Powered by Bridg, this initiative is a partnership with Universal Media Inc. aiming to provide unique insights, create tailored audiences, and execute unified campaigns across multiple retailers. The product focuses on transparent measurement of advertising spending’s impact on sales. Rippl is said to focus on providing first-party data to previously unattended regional retailers. In addition to product launches, Cardlytics also sold Entertainment to Kigo. Entertainment was bought for 14.6M€ in late 2021 to provide local offers focusing on local restaurants. The price of the deal was undisclosed but will be quantifiable once Cardlytics posts its Q4 2023 results. Ironically, Augeo, the former parent company of Figg was the acquirer.

Given the pivot towards larger advertisers and cost control, management may prefer to have the cash in hand. However, I will note that the real money for this business is in the local and regional Small and Medium Businesses (SMBs) offers. As outlined in previous letters, SMBs are at the core of stage three of the thesis and would require management to focus on self-service and aggregation.

Interviews and Insights

These past 6 months have been filled with client and partner interviews. Your PM has gone through various transcripts mostly provided by a major investor acting as a host, in search of relevant information that could modify the investment thesis. The interviews are centered around the pros and cons of working with Cardlytics. The items discussed served as both strong proof of concept and valuable feedback on areas where the company is struggling. I will focus on the latter point as it serves as a way of keeping score on critical items that Cardlytics has to either build or work on.

1. Overall attribution and testing: the overall sentiment of smaller advertisers has been skepticism on the results front. A few clients commented on the fact that campaigns take too long to get verified and, even when verified, the results are seen as more trust-based than data-based. Many advertisers reported getting weekly updates on campaign results with incrementality shown only after the campaign was completed. Personally, I don’t believe most advertisers understand randomized control trials. Most people in marketing departments are used to Multi-touch Attribution (MTA) models which are commonly promoted by the two main players aka Google and Meta. MTA has its own set of issues, but it can provide instantaneous estimated results and these seem to be the preferred choice for advertisers. Additionally, the data provided by Cardlytics at times cannot be processed by advertisers to the degree that they want or using the format that they are familiar with.

2. Geo-lift validation: this item is a robust way of testing data and was demanded by clients on multiple occasions according to the statements within the interviews. The test consists of providing a selection of locations (cities, states, regions, countries, etc.) with a marketing campaign while depriving another location of this same campaign. After a select period, a variety of business metrics are measured on both locations to determine whether the campaign was effective and what the incremental value was. It is a correct testing point, but in the case of Cardlytics, it only accounts for one of many variables it takes into consideration. However, because of its popularity, this is requested and done selectively by Cardlytics for customers with a larger budget. For smaller clients this is likely not the case, which adds weight to the argument of perceived uncertainty of results.

3. Minimum budgets: the previous point leads to having a chicken and egg problem whereby advertisers will not spend more without getting more testable data, and Cardlytics won’t present this data unless advertisers spend more than a certain threshold (seems to hover around 3M USD/year).

4. Definitions and goals: additionally, advertisers seem to have different priorities when it comes to selecting targets. The main difference stems from the definition of incremental value. For some advertisers, former customers who had not acquired the product a long time ago do not count towards incremental value as they are not new customers per se. Cardlytics has been adapting partially to this by discarding users based on email lists, however, in terms of real incrementality, the difference should reside on whether the person would’ve or wouldn’t have purchased the product without the provided incentive.

5. Auditing results: currently the results from campaigns and data usage are audited by a third party. Cardlytics has chosen Nielsen to carry out this task. Even though Nielsen is a leader in the field of communications and data analytics, for a smaller advertiser who’s unable to test data it might sound too obscure. On the one hand, results for larger advertisers are provided with a higher level of detail, meaning that Nielsen’s verification services are not why they trust Cardlytics. On the other hand, smaller advertisers, having less information, would be more comfortable with e.g. a Big Four accounting firm.

6. Dashboards and communication: Figg, the competitor acquired by JP Morgan to sustain the data analytics capabilities of their SMB clients has recently launched a dashboard. Competitors like Figg or Amex seem to have better reporting capabilities and thus can be perceived as a better option or at least build trust with many more advertisers. The simplest way for non-technical marketers to understand the results of their budget allocation decisions is by providing exactly this feature. If a non-technical decision-maker can visualize how a certain amount of money can perform, that individual should be more likely to spend towards true maximization as it can compare services across its providers using a similar measurement system (simplifying iROAS vs ROAS).

To sum up the previous points, I believe that Cardlytics issues hover around two pain points. One is making data-based decisions digestible, and the other is reducing time-data-related frictions. On the first pointer, Cardlytics needs to provide a simpler and more visual approach to data. On the second pointer, Cardlytics needs to reduce test/reporting times and provide testable data in a format that marketers are more familiar with. I believe management is hard at work addressing both points. All this being said, in an ideal future marketers learn from the scientific approach provided by Cardlytics as it is much healthier for their marketing budgets. Cardlytics is certainty while its competitors are a promise that may or may not be true. For the time being, this results in single to low double-digit budget allocations towards Cardlytics, but this could drastically change with the proposed changes.

Key personnel

There has been quite a lot of movement when it comes to new talent being hired by Cardlytics. As pointed out by Karim (CEO) in past statements, he has a list of candidates for core positions at the company but is dependent on the share price to execute. Great talent costs money and management prefers not to dilute shareholders especially while the price of the shares is low. Here is a short list of key individuals who have been part of the hiring/appointment spree, I would recommend reading their bio on the official Cardlytics page:

Ending note

As an ending note, I had the chance to ask the RV Capital managers a question on Carvana and AdTech (applicable to Cardlytics). You can listen to their answer here or on YouTube by searching for “Investor Q&A - Rob Vinall and Andreas Lechner answer questions about Business Owner Fund's 2023” (minute 23:00). Andreas took on the AdTech question and responded to the following (paraphrased):

The conclusion from thorough research is to avoid the technology providers and instead invest in platforms. Technologies are prone to disruption, but platforms can control the information, and their usage is driven by network effects. Third-party banner providers have a hard time adjusting when newcomers enter the sector. Platforms too are forced to adapt to new competitors, but they are hard to disrupt because of these same network effects.