🧗 Top 5 NEW Companies from Planet Microcap

OIJ (#28) Breaking Down a Few Standout Public Companies

Welcome back dear fellow 🧙♂️ Hermits 👋

🧙♂️ First time here? → This 3-Minute Crash Course Will Save You Hours

📈 We Think This Company Could 10x → Full Breakdown Inside

💼 What We’re Buying, Holding, and Cutting → Portfolio Update Live

Index

📋 Brief Overview

💼 Kingsway Financial Services ($KFS)

🌐 NameSilo ($URL)

🏥 Nova Leap Health Corp ($NLH)

🕵️♂️ Red Violet ($RDVT)

🔬 Sanuwave ($SNWV)

🎁 Bonus Content

None of the following should be construed as investment advice. Please consult a financial advisor before making any investment decision. You will find a full disclaimer at the end of this post.

📋 Brief Overview

As many of you know, we recently attended Planet MicroCap in Las Vegas, and we walked away seriously impressed.

The event delivered on every front. The quality of attendees (both company execs and fellow investors) was top-notch. Add to that a super well-run setup that encouraged real conversation and constant info flow, and you’ve got the perfect storm for deep dives and conviction building.

So… we’re bringing you our Top 5 Standout Companies from the conference. Each one earned its spot for different reasons, and we’ll walk you through them in quick, info-rich pitches (think ~5-10 minutes each).

Here’s how we’ve structured it:

What they do – a brief, clear overview

Why they made the cut – the key hooks that caught our attention

Valuation snapshot – with a few highlights (and red flags) you’ll want to know

Let’s begin…

💼 Kingsway Financial Services ($KFS)

KFS is a holding company pioneering a scalable version of the search fund model, offering centralized back-office support and permanent capital to entrepreneur-operators.

The company provides succession solutions for small business owners by enabling primarily MBA-trained operators to acquire and lead businesses. In doing so, KFS functions both as a fund-of-funds and an accelerator, streamlining the search, acquisition, and operational transition process under one roof.

Failure rates in search funds are comparable to those in venture capital, roughly 50% of projects either break even, fail to return original capital, or don’t make it past the search phase.

At first glance, this might seem like a red flag. However, the underlying dynamics of the asset class tell a different story. Competition for quality deals remains remarkably low, and when acquisitions do happen, the upside can be exceptional.

In 2024, the asset class delivered a 35.1% IRR across all search funds (worldwide, with EU returns being better than those in NA), with exited deals generating an average IRR of 42.9%.

We’ve reviewed dozens of these models ourselves, especially during 2023/24 when we nearly launched our own accelerator. If you’re interested in digging deeper into the data, the definitive resource remains the latest Stanford Search Fund Study. You can find the full report here:

Back to KFS… searchers are typically compensated around $125k annually for up to two years (with occasional exceptions extending to three). Once sold, they can earn a success fee (ranging from 3% to 25% of gains) structured as carry and tied to the internal rate of return (IRR) generated.

That IRR, in turn, depends on five variables:

purchase price

exit price

growth in profitability (rather than top-line revenue)

leverage employed, and

holding period

KFS mitigates risk by capping purchase multiples and applying a standardized 50/50 debt-to-equity structure. Execution, operational upside, and eventual value creation remain primarily in the hands of the searcher.

KFS currently owns a portfolio of operating businesses and is actively backing three searchers, with a growing pipeline of future operators. By building out this talent pipeline and centralized infrastructure, the company increases its odds of success, both at the individual deal level and as a long-term compounding holding company.

At the heart of KFS’s model is the belief that alpha lies in two things: disciplined sector selection and decentralized execution. They aim to identify industries with asymmetric return potential and empower operators to drive results independently within that framework.

Each acquisition is structured as a standalone entity with its own balance sheet, ensuring clear accountability. KFS provides permanent equity capital to support these acquisitions, while debt is raised at the deal level. This separation balances autonomy and oversight, creating an ecosystem of accountable entrepreneurs backed by long-term, flexible capital.

The use of permanent capital enables longer holding periods, essential for compounding to occur. It also creates optionality for follow-on investments or targeted roll-up strategies within individual SPVs, transforming successful operators into potential platforms.

Why Do We Like It?

You’ll probably notice a recurring theme across all the companies we highlight, but it’s worth repeating: execution is everything. In the world of smaller companies, it all comes down to people. And KFS has some top-tier talent.

We had a highly productive conversation with both CEO John T. Fitzgerald and CFO Kent Hansen. Judging by the tone and depth of the discussion, both sides came away impressed with each other.

While most conference conversations likely revolved around near-term financials and the pipeline of upcoming searchers with questions like “What’s your next quarter look like?”, as you can probably guess, ours didn’t touch a single number.

We focused exclusively on process.

John Fitzgerald, for one, has a serious track record. After graduating from Northwestern, he launched multiple ventures, including his own search fund. His responses to nuanced questions showed deep sector knowledge and composure… traits that set exceptional operators apart.

Frankly, yes, he’s someone we admire.

CFO Kent Hansen offered valuable insight into the internal structure. Back-office tasks like accounting and compliance are centralized and executed by what appears to be a highly competent in-house team, delivering top-tier services at a fraction of market cost.

Still, day-to-day operations remain entirely in the hands of each individual company’s management team, led by the searcher-turned-CEO.

One standout structural element is the supervisory board: a small, high-caliber group that doesn’t micromanage but nudges companies in the right direction. All companies share a single centralized board. The fact that someone like William Thorndike sits on that board speaks volumes.

KFS’s architecture allows for aggressive growth without structural fragility. Adding new companies simply means modestly expanding the centralized back office while preserving full autonomy and accountability at the deal level.

If one project fails, there’s no contagion risk. The mothership moves on, unharmed.

Now for the personal bit. If I wasn’t running a fund, I’d probably want to work with these guys. What they’ve built isn’t just operationally sound, it’s brave.

Anyone who’s tried building something complex knows how much friction hides in the most minute details. And I’m willing to bet a thousand people told them this model wouldn’t work. That’s conviction. Hats off to them.

What’s It Worth to Us?

Valuing KFS is inherently tricky.

Much of its cash flow comes from divestitures, and linking that to current holdings is difficult, especially given that the reported numbers include a lot of embedded growth, making anything beyond a two-year forecast speculative at best.

A rough sum-of-the-parts suggests the current portfolio might be worth around $200 million. But take that with a grain of salt. We're the first to admit we’re not SOTP experts, we pretty much suck at it. Additionally, we won’t share the exact calculation as we prefer not to share individual data points. You’ll have to trust us on this one.

That said, we wouldn’t be surprised if a few standout deals dramatically move the needle. The model scales beautifully, so there’s no meaningful ceiling on potential upside. Plus, the team seems to be in it for good.

The company also carries significant NOLs (net operating losses), or tax assets, which management claims could hold substantial value. That said, we’ve rarely seen these fully realized, especially in cyclical businesses where exit timing is largely out of their control.

One area we’re less enthusiastic about is the structure of the preferred shares, which carry an 8% dividend and are convertible into common equity. It’s an expensive form of capital.

While the overall issuance is “limited”, it still represents dilution and a drag on long-term compounding. Simply put, it’s not our favorite financing decision.

Overall grade: 8/10

🌐 NameSilo ($URL)

URL is a domain registration and web services platform that offers customers global domain management, hosting, email, and security services. However, its core user base remains concentrated in the U.S. and Canada.

At first glance, it may appear to be a low-growth, commoditized business. But dig a little deeper, and you’ll find a remarkably resilient cash-flow compounder with layers of optionality thanks to its low churn, sticky revenue, and a management team that understands capital allocation.

As of 2024, NameSilo managed over 5.7 million domains across 160 countries and remains among the top 15 registrars globally. What’s compelling here is that despite its modest size, the business punches above its weight regarding cash generation and capital efficiency.

The domain registration industry is often dismissed as brutally competitive and margin-thin, but that misses the real story: retention. Industry renewal rates typically hover around 85–90%, and NameSilo itself reported a domain renewal rate of approximately 87% back in 2019 (source). That kind of stickiness creates an annuity-like revenue stream that’s difficult to disrupt once domains are locked in.

While acquiring a domain name often costs less than $20, what’s more important is the renewal dynamic. Customers frequently pay for multiple years up front (2-5 years), leading to substantial deferred revenue.

For operators like NameSilo, that translates into prepaid cash that they can reinvest. This front-loaded cash model gives the company ample flexibility to fund operations, invest in product extensions like hosting or SSL certificates, or opportunistically buy back shares and pursue M&A, something management has experience with.

Why Do We Like It?

At the helm of this quietly compounding machine is none other than Paul Andreola, a name that carries serious weight in Canadian microcap circles. We won’t go so far as to say everything he touches turns to gold, but the track record speaks for itself: companies he backs tend to outperform, often massively, once the market catches on.

Andreola is a sharp capital allocator, deep-dive researcher, and operator who understands the nuances of small company inflection points better than most. He built his reputation identifying under-the-radar businesses with real earnings, durable economics, and hidden growth levers long before they show up on institutional screens.

If you’re unfamiliar with his approach or just want to hear how he thinks about investing, we highly recommend this podcast episode:

It’s a masterclass in microcap investing. Think quiet compounding, insider alignment, and the art of patience in a short-term world.

…Or, better yet, check out their website, where Paul and Trevor Treweeke regularly highlight standout companies, niche sectors, and overlooked investing themes in depth. It’s just well-researched ideas from two guys who actually walk the talk.

And just to be clear: this isn’t a paid promo. We’re just genuine fans of the work they put out. 😉

What’s It Worth to Us?

The core business is currently generating approximately $10 CAD million in free cash flow. Based on industry trends and NameSilo’s current trajectory, we believe the company can grow revenues organically at ~10% per year, in line with its 5-year CAGR of 13.6%, and excluding the tailwind of inflation.

Domain registrations alone have grown at a 9.1% CAGR over the same period. Given the company’s highly scalable model, where variable costs are minimal, this growth translates almost entirely to the bottom line.

Unlike other holding companies like KFS, NameSilo’s portfolio is relatively simple and can be broken down cleanly. (And yes, just a friendly reminder: all figures are denominated in fake money 😊 aka Canadian dollars.)

a. Liquid Public Holdings + Bitcoin

The largest portion of the portfolio is allocated to listed assets:

Bitcoin (8 units) → Valued at $130,000 each, totaling $1.04 million

Atlas Engineered Products (971,079 shares @ $0.81) → $786,574.

ImmunoPrecise Antibodies (557,500 shares @ $0.70) → $390,250

West Mining Corp. (18,000 shares @ $0.05) → $810.

These public assets total $1,177,634 plus the Bitcoin, that’s a total of $2,217,634.

b. Private or Super Illiquid Equity Positions

This section of the portfolio includes stakes in private companies or very thinly traded names:

Allur Group (523,333 shares) → $78,500.

Ceapro Inc. (1,746 shares) → $6,740.

Domai Technologies → $47.

Combined, these assets amount to $85,287.

c. Venture Assets

Yuansfer → A payments or fintech-related investment valued at $63,390.

Bomb Beverages → A beverage company stake marked at $32,387.

These are valued under Simple Agreement for Future Equity rules. They total $95,777.

The total portfolio is worth $2,398,698 as of May 14th.

We also get the benefit of a steady, opportunistic share repurchase program. The company bought back 637,500 shares in 2023, followed by 907,500 shares in 2024, steadily reducing the basic share count over time.

This doesn’t yet factor in the preferred shares issued in 2024 (check diluted figures below).

And to top it off, we have the ultimate wildcard: Paul Andreola as the capital allocator. He’s known for being highly selective and opportunistic, with a track record of uncovering and backing overlooked gems. His involvement adds a layer of strategic optionality.

How much would we pay for this?

Using our go-to sanity check of 15% FCF yield, this implies a valuation of:

2025 valuation = ~6× C$11M of FCF = C$66M + C$2.5M portfolio = C$68.5M

2026 valuation = ~5× C$12M of FCF = C$60M + C$3.0M portfolio = C$63M

Overall grade: 8/10

🏥 Nova Leap Health Corp ($NLH)

Nova Leap is a home healthcare provider specializing in at-home dementia care and senior support across North America.

Unlike traditional healthcare providers that centralize care in facilities like nursing homes, hospitals, or hospice centers, Nova Leap is built around a different philosophy: helping people remain in their homes for as long as possible.

That’s not just their approach, it’s their mission statement:

The company operates across North America, executing a classic consolidator strategy: acquiring smaller local operators and centralizing back-office and administrative costs to unlock efficiencies.

Their acquisition criteria are straightforward and fairly disciplined:

Private-Duty Non-medical Home Care focus;

Revenue sources are primarily composed from private pay, Veterans Affairs, or Long-term Care Insurance (little to no Medicare/Medicaid);

Non-franchised;

Generating at or above $1.5 Million (USD) in annual revenue; and

Located in the United States or Canada.

The idea looks solid at a high level, but it's up against a few structural headwinds. The biggest challenges come from scalability, customer recurrence, employee availability, and regulatory hurdles.

By nature, the model is hard to scale. Unlike centralized care facilities, this approach requires sending caregivers directly to patients’ homes, which introduces logistical friction. Range is a real issue.

Caregivers often have to travel between multiple locations, limiting their efficiency. As a result, weekly schedules usually cap out between 36 and 44 hours.

On top of that, while the hourly cost to clients is relatively low (~$30/hour), the economics are tight. There’s a growing shortage of social and care workers, which is pushing wages up, but those higher costs are tough to pass on to the client, who is often the adult child of the person receiving care and already under financial pressure. Inflation didn’t help either.

In short, while the concept makes intuitive sense and serves a real need, there are some very real frictions when it comes to scaling it profitably.

Why Do We Like It?

We love a good ol’ consolidation play. The strategy here is dead simple: scoop up small mom-and-pop operations using mostly cash (plus a sprinkle of promissory notes here and there, usually representing 10–20% of the deal value).

These targets are typically small offices in strategic parts of the city, run by a tight crew: five staffers in the office, a couple of nurses, and a team of caregivers under permanent or semi-permanent contracts. They must have a steady set of local clients they serve regularly.

Keep in mind, these folks are in a business where death is a regular part of the job, so understanding customer turnover and (business) lifecycle dynamics is absolutely critical.

To keep things clean, we’re sticking to aggregate yearly multiples except for 2025. You can reverse-engineer the rest if you’re feeling curious, but trust us: the year-by-year snapshot paints a pretty clear picture.

2025

(MacDonald Home Care, Nova Scotia) May 2025 - $1.1 million and adjusted EBITDA of approximately $95,000 for its 2024 fiscal year. $390,000 total, paid cash on close.

(Earth Angels Home Care, Nova Scotia) January 2025 - Paid $1,005,725, expected annualized $456k increase in revenue and $50k in operating marginn

2024

▸ Revenue Added: $4.0M

▸ Operating Income Added: $410K

▸ Total Paid: $1.89M

▸ Multiples: 0.5x revenue / 4.6x operating income

(Life Home Health, Florida) December 2024 - Paid $1,596,716

(Tender Hearts Home Care, Massachusetts) May 2024 - Paid $296,067

2021

▸ Revenue Added: $10.9M

▸ Operating Income Added: $1.53M

▸ Total Paid: $8.51M

▸ Multiples: 0.8x revenue / 5.6x operating income

(Carestaf, Texas) December 2021 - Paid $1,643,226

(Eldercare 4 Families, Kentucky) December 2021 - Paid $4,727,212

(Care for Life, South Carolina) December 2021 - Paid $545,906

(My Choice In-Home Senior Care, Oklahoma) September 2021 - Paid $1,075,500

(All is Well Home Care, Rhode Island) July 2021 - Paid $520,895

2020

▸ Revenue Added: $4.46M

▸ Operating Income Added: $400K

▸ Total Paid: $2.44M

▸ Multiples: 0.5x revenue / 6.1x operating income

(Family Bridges Home Care, Ohio) December 2020 - Paid $1,080,979

(Curtin Home Care, Massachusetts) October 2020 - Paid $1,114,404

(Around the Clock Home Care, Arkansas) September 2020 - Paid $248,577

2019

▸ Revenue Added: $2.35M

▸ Operating Income Added: $329K

▸ Total Paid: $1.48M

▸ Multiples: 0.6x revenue / 4.5x operating income

(Keystone Home Care, Massachusetts) November 2019 - Paid $375,000

(Around the Clock Home Care, Oklahoma) October 2019 - Paid $578,790

(Careforce Home Care, Nova Scotia) April 2019 - Paid $523,006

2018

▸ Revenue Added: $5.14M

▸ Operating Income Added: $295K

▸ Total Paid: $7.51M

▸ Multiples: 1.5x revenue / 25.5x operating income

(Armistead Senior Care, New Hampshire) October 2018 - Paid $419,064

(Comprehensive Home Care, Massachusetts) September 2018 - Paid $1,569,423

(Always Home Homecare, Nova Scotia) June 2018 - Paid $2,263,676

(Home Health Solutions, Massachusetts) April 2018 - Paid $1,186,792

(Family Tree Home Care, Massachusetts) February 2018 - Paid $2,074,950

2017

▸ Revenue Added: $3.65M

▸ Operating Income Added: $49K

▸ Total Paid: $2.20M

▸ Multiples: 0.6x revenue / 44.9x operating income

(All About Home Care, Rhode Island) September 2017 - Paid $1,200,000

(Armistead Senior Care, Vermont) October 2017 - Paid $1,000,000

2016

▸ Total Paid: $240,000

▸ Implied Annualized Revenue Increase: $392,000 (10 months of data)

▸ Implied Operating Income Added: $5,000

(Armistead Senior Care, New Hampshire) October 2016 - Paid $240,000

With all this data in mind, it’s clear the company has evolved… from scooping up scrappy “fixer-uppers” to acquiring more mature, consolidated operations.

The strategy seems focused on paying around 0.5x–0.6x revenue and 5x–6x operating income, aiming for a solid return on capital. And thanks to a bit of operational fine-tuning and only light use of debt (they rarely use leverage for acquisitions), those effective multiples are likely even lower in practice.

What’s especially impressive? All M&A is done in-house. That’s a major green flag and suggests real specialization and repeatability. CEO Christopher Dobbin brings the chops, with over 15 years of investment banking experience, much of it focused on healthcare transactions. The M&A team is lean (just three people), and Christopher himself still handles the bulk of the work.

Their acquisition criteria are also crystal clear: target companies with 10–15% operating margins. Christopher confirmed this directly and even noted that employees are incentivized to maintain or improve those margins, a structure that drives accountability and efficiency at the local level.

The result? A highly decentralized model with tightly aligned incentives, where each center’s performance actually matters.

Management alignment is another bright spot. Insiders collectively own ~40% of the company. The two largest stakes belong to the estate of Norman Wayne (20%) and Christopher Dobbin (10%).

Interestingly, there’s a clause in Norman Wayne’s estate that mandates a sale only if Christopher sells — so unless he walks, that chunk is essentially a locked-in, permanent shareholder. Of course, that also means any sale from Christopher could trigger… well, a bit of a mess.

The remaining insiders hold about 10%, so in practice, the true float is tiny. While the market cap may show C$21M, the tradable equity is closer to C$12–13M.

Also, if you haven’t already, we highly recommend reading their latest Letter to Shareholders. It gives a great sense of where the business is heading.

What’s It Worth to Us?

With all acquisitions to date, the company is now generating around C$30 million in revenue. With effective consolidation, that should translate into roughly C$3 million in EBIT — a 10% margin. It’s worth noting that course-correcting underperforming operations has been more effort-intensive in earlier deals, but this burden has eased significantly with more recent, higher-quality acquisitions.

The key questions now are: How fast can they grow? And what will it take to get there?

So far, the company has taken an opportunistic approach to M&A, but internally, they target around 3 to 4 acquisitions per year. If they can consistently add C$4–5 million in revenue annually, that equates to C$400–500K in additional EBIT, assuming similar margins.

Based on past deal terms, that level of growth would likely require C$2.5–4 million in capital per year, implying a 5–10 year payback period. Not the best, but also not bad for a roll-up in a sticky, regulated industry.

On the balance sheet front, the company remains conservative. It has C$2 million in net debt, with minimal long-term liabilities. While it has occasionally issued equity to fund larger deals, it’s also actively managing dilution, recently buying back about 5% of its shares (from 86.8M in 2024 to 82.7M as of March 2025).

So… where does that leave the company?

We’d estimate C$35 million in revenue for 2025, up from around C$30 million in 2024. Applying their target margins, that should translate to C$3.5–4.0 million in free cash flow, enough to start self-financing future acquisitions.

We wouldn’t be willing to pay more than ~6× estimated 2026 FCF, which puts our valuation cap at around C$24 million.

The company appears to be right at the tipping point: give it another year or two of modest debt support, and it could shift into cruise control, compounding organically without external funding.

Whether they stick the landing remains to be seen… but from where we’re sitting, it’s shaping up to be a very attractive compounding machine.

Overall grade: 8/10

🕵️♂️ Red Violet ($RDVT)

RDVT is an identity intelligence and analytics firm serving the world of compliance, fraud detection, and risk management. In simple terms, they help track down people who owe money, minus the mob-style chasing down with a baseball bat, unfortunately 😉

Their core product is a platform called IDI, which allows users to digitally trace individuals and their assets. It gives organizations much-needed visibility when it comes to a wide range of use cases: background checks for employment or immigration, lending decisions, criminal investigations, insurance underwriting, risk assessments, and even verifying the ownership and value of hard assets like real estate.

The company operates in a space that’s close to our hearts (cybersecurity), and it’s one that’s come up in conversations with us multiple times over the years. Back then, we were exploring potential partnerships. But now that we’ve made the shift to full-time investing, we’re looking at it through a different lens: ownership.

Why Do We Like It?

Unlike every other company on this list, we haven’t met management yet to fully close the loop. That said, the idea is so mission-critical to our space, and the execution so strong so far, that we’re compelled to take a serious look regardless of whether we’ve had the handshake or not.

For this one, we’re leaning on our own experience and the macro trends we've tracked for the better part of the last decade. There’s a clear cycle: as security improves, criminal and deceptive behavior evolves in complexity. This cat-and-mouse dynamic forces companies, especially larger institutions, to adapt or fall behind.

In that context, RDVT’s solution stands out. It’s simply too efficient and too cost-effective to ignore. For most organizations, it’s not worth the time, money, or talent to try and build this kind of infrastructure in-house. And the return on investment is compelling — we’re talking 1:8 to 1:12 for things like collections and high-precision risk assessments.

Put simply, it’s a no-brainer for institutions that need accuracy, speed, and scale.

This is what we see on the pros side of the equation:

1. Mission-Critical Product (IDI Platform) → RDVT’s core product, IDI, is used by professionals in fraud, compliance, risk, and law enforcement. It helps uncover and verify identities, track down assets, and assess risk, making it essential infrastructure in the digital age

2. High-Margin, Scalable SaaS Model → The business operates with a high-margin software model. Once clients are onboarded, incremental costs are low and operating leverage kicks in quickly, allowing FCF to scale rapidly with revenue

3. Recurring Revenue from Sticky Clients → RDVT serves sectors that depend on ongoing access to identity data, like debt collection, insurance, legal, and government. These clients typically integrate IDI deeply into their workflows, resulting in high retention and recurring revenue

4. Tailwinds from Growing Fraud and Compliance Needs → In a world of increasing fraud, financial crime, identity theft, and regulatory scrutiny, demand for identity intelligence is only going up. RDVT is riding this wave with a focused and specialized solution

5. Proprietary Data + Analytics = Moat → RDVT has built a proprietary database infrastructure and analytics engine that are difficult to replicate. Its data sourcing and matching capabilities offer real-time accuracy that competitors struggle to match, giving it a defensible edge

6. Strong Use Cases Across Verticals → Use cases include employment screening, tenant vetting, insurance fraud detection, legal investigations, asset tracking, and financial risk assessments. This gives RDVT exposure to multiple end markets and reduces concentration risk

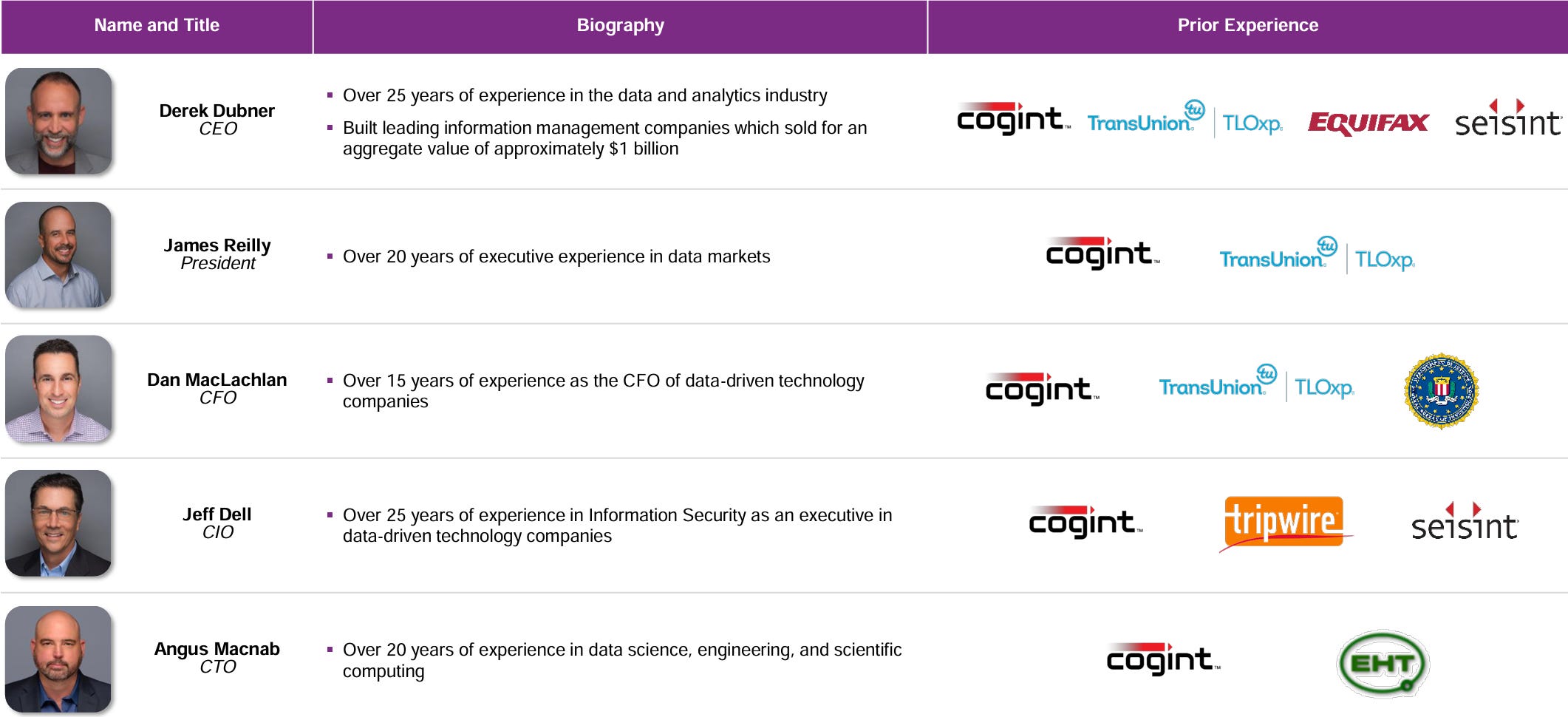

7. Founder-Led with Insider Skin in the Game → Management, led by CEO Derek Dubner, has significant insider ownership (3.7%). The company was spun out of Cogint (pretty good company) and built deliberately over years

8. Zero Debt and a Healthy Balance Sheet → RDVT has no debt and ample cash, giving it flexibility for M&A, R&D, or opportunistic repurchases. That financial conservatism is a plus in volatile markets.

9. Undervalued Relative to Peers → Compared to other identity and risk analytics companies (Verisk, TransUnion, RELX, or even Palantir in broader intelligence), RDVT trades at a significantly lower multiple, despite similar tailwinds and business quality.

10. Optionality for Government or Strategic Partnerships → With growing regulatory needs and national security concerns around digital identity, RDVT’s tech could eventually become a prime acquisition target for strategic buyers or defense-related entities looking to expand capabilities.

So why not just go all-in on this?

We’ve thought long and hard about it, and the biggest concern boils down to GDPR and data privacy. In a world where personal data misuse or leakage can instantly destroy reputations, this is no small risk.

While RDVT operates as a third-party provider, which allows clients to shift some of that risk onto them, it also means RDVT could be carrying more liability than they can realistically handle, especially if regulators or courts decide to make an example of someone.

What’s It Worth to Us?

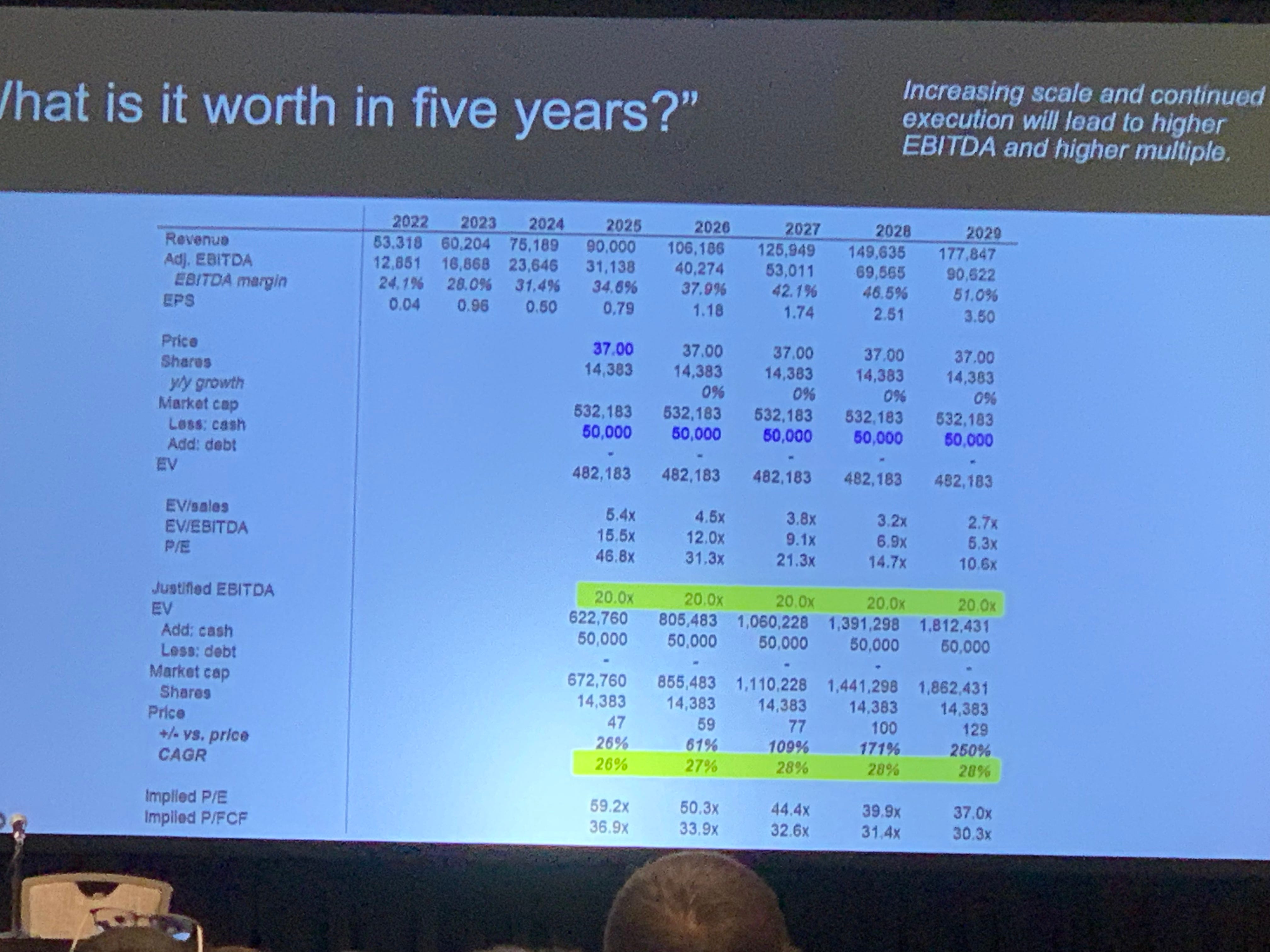

Better minds than ours performed a valuation, and this is what they got:

To keep it simple: our target price for 2025 is $47 per share, implying a $670M market cap. For 2026, they see a fair value closer to $59 per share, or about $855M in equity value.

We won’t pretend to have a better valuation model as we’re still early in understanding how quickly the products can scale, the strength of the pipeline, and how the backlog converts.

That said, from a "cheap bastard" perspective, the current valuation is a tough pill to swallow.

At a $650M enterprise value, the stock is trading at ~26x LTM FCF and ~65x LTM EBIT (as of Q1 2025). To justify those multiples, we’d need to see very consistent 25%+ annual revenue growth (aka doubling every three years) and EBIT margins pushing toward 40-45%.

Overall grade: 9/10

If you’d like to dive into the full presentation from Planet Microcap, you can check it out here:

🔬 Sanuwave ($SNWV)

SNWV is a medical device company developing non-invasive shockwave therapy for chronic wound healing.

The company has about 140 patents and has developed 2 products to date: UltraMIST® System and dermaPACE® System. Being honest, dermaPACE is completely irrelevant, and the company plans on discontinuing this line and focusing on UltraMIST and possibly version 2.0 of this product.

From the interpretation brought to my attention by specialists, this, their star product, is significantly better and cheaper (about 50% of the price for a treatment) than traditional alternatives.

The UltraMIST System is a non-contact, low-frequency ultrasound therapy device designed to accelerate wound healing. It delivers ultrasound energy through a fine saline mist, allowing the treatment to reach the wound bed without the applicator ever touching the skin.

This non-invasive approach reduces the risk of further trauma or contamination, making it particularly well-suited for chronic or fragile wounds (plus it’s painless).

Mechanistically, the system operates at around 40 kHz, producing ultrasound waves that travel through the mist and penetrate the wound tissue. This stimulates a range of biological responses: it reduces bacteria and biofilm on the wound surface, enhances blood flow (perfusion), decreases inflammation, and promotes angiogenesis (formation of new blood vessels).

Collectively, these effects support faster and more effective healing in both acute and chronic wounds, including diabetic foot ulcers, pressure ulcers, venous leg ulcers, and post-surgical wounds.

Treatments typically last between 3 and 12 minutes, depending on wound size, and are applied two to five times per week. The ease of use and non-contact nature of UltraMIST make it a strong option in both outpatient and home-care settings, especially for patients with high infection risk or pain sensitivity.

When compared to other advanced wound care technologies, UltraMIST stands out for its non-contact delivery. For instance, Negative Pressure Wound Therapy (NPWT) applies suction through a sealed dressing to promote granulation tissue, but it involves bulky equipment and requires frequent dressing changes. Electrical Stimulation Therapy (e-stim) uses electrodes to apply current that stimulates cellular activity, but it requires direct skin contact and isn’t always suitable for all wound types. Hydrotherapy, including whirlpool or pulsed lavage, is useful for cleansing wounds and removing debris, though it’s less precise and increasingly seen as outdated due to infection risk.

We found their investor deck insightful. You can check it out here:

Why Do We Like It?

This is by far the most volatile name on the list, and the reason for this is that it comes down to one person: Morgan Frank.

He’s a very energetic investor with deep expertise in healthcare and surgical devices. This is his track record of deals and exits in the space:

Think of someone who doesn’t just understand the space he moves within it like a shark. Precise. Relentless. Super freaking dialed-in.

Fortunately, we had the chance to interview him, with support from a Toronto-based social worker (potential user) and a New York–based commercializer of medical devices (potential salesperson). They have a much deeper understanding of demand/supply dynamics than we do.

To give you a sense of the direction we wanted to take the conversation, here’s a snapshot of the questions we prepared ahead of the interview:

How do you perceive the risk of depending (90% rev) on a single product?

What wound types see the strongest clinical response with UltraMIST — diabetic foot ulcers, pressure ulcers, surgical wounds?

What’s the unique clinical value proposition of ULTRAmist vs dermaPACE vs. competitors?

Of the devices placed, what percentage are actively used in routine patient care? What are the key reasons for non-use?

How does UltraMIST fit into clinic workflows today? Are staffing or time requirements a barrier?

What’s the average number of treatments per wound or per patient? Is UltraMIST a one-and-done device or used across long treatment cycles?

What is the current Medicare coverage situation? Are there CPT codes in place for the products, and what’s the average reimbursement rate?

What is the CMS coverage status for UltraMIST? Is it bundled under wound care episodes or separately reimbursable?

Are there any foreseeable risks to coverage or billing codes that could impact utilization?

Beyond IP, what prevents hospitals or clinics from switching to a cheaper or simpler modality?

In 3 years, do you see UltraMIST as your flagship product, a stepping stone, or part of a larger integrated wound care platform?

They’ve not done marketing, but will they start now?

Needless to say, we barely stuck to the script.

The conversation quickly shifted toward Morgan’s prior experience and the broader activity of his hedge fund, Manchester Management (Explorer Fund).

We covered everything from past activist strategies to the before-and-after story of Sanuwave, and what ultimately led him to step in as CEO. He also spoke about his partner's role as CEO of another portfolio company, and hinted at what’s coming with UltraMist 2.0.

The conversation was incredible, easily one of the most engaging we’ve had, especially given that stepping into an activist role is something I’d personally love to do with a portfolio company someday.

That said, I didn’t exactly play it straight. I kept offering this athlete sugar in the form of some dangerously good macarons, teased him about his family situation (no wife, no kids), bonded over our shared background in wrestling, and pushed him on a big one: his definition of success.

Mr. Frank is a double-edged sword.

He’s either ruthlessly extracting every ounce of value before winding the company down, or he’s in it for the long haul, reinvesting every dollar into building an exceptional second-generation product.

There will be no middle ground. Just pure conviction, one way or the other.

Note that they also raised money for a few additional ideas in February 2025.

What’s It Worth to Us?

This is arguably the hardest company to value, precisely because of the projected growth curve. Management is guiding for $48–50 million in revenue for full-year 2025, and while those figures appear realistic, the real story lies in the backlog buildup. That’s what will ultimately drive visibility and valuation.

The business operates on a classic razor-and-blade model. Devices are sold for $35,000 apiece, while single-use applicators go for $100 each. Gross margins on both hover around 75%.

To date, the company has done virtually no marketing. These changes will occur in the second half of 2025 (confirmed). Let’s walk through a quick (but telling) back-of-the-envelope exercise.

📦 Device Sales

There are currently 1,047 devices in the field, with 374 units sold in 2024, implying 55% YoY growth. They can now produce 100–120 units per month. Let’s conservatively assume:

2025: 700 units sold → $24.5M revenue

2026: 1,000 units sold → $35.0M revenue

🔁 Applicator Sales (Recurring Revenue)

As of March 2025, weekly production capacity for applicators is 10.5k units. By year-end, they expect to scale to 24k/week, and up to 32k/week in 2026. User feedback suggests they can sell 100% of production, but to stay conservative, we’ll model 80% sell-through:

2025: 20,000 units/week × 52 weeks × $100 × 80% = $83.2M revenue

2026: 32,000 units/week × 52 weeks × $100 × 80% = $133.1M revenue

It's worth noting that applicators, in particular, are likely to be purchased in bulk and financed. This implies deferred payment terms and the potential for per-unit discounts, especially from institutional buyers acquiring large quantities.

📊 Sales & Margins

2025 Total Revenue = $24.5M (devices) + $83.2M (applicators) = $107.7M

2026 Total Revenue = $35.0M (devices) + $133.1M (applicators) = $168.1M

They’ve already reached 20.6% LTM EBIT margins (up from breakeven), but 30–40% is well within reason given operating leverage.

Using a conservative 35% margin:

2025 EBIT: 35% of $107.7M = $37.7M

2026 EBIT: 35% of $168.1M = $58.8M

📈 Valuation

Assuming EBIT ≈ FCF (light reinvestment needs), and targeting a 15% FCF yield, that implies:

2025 valuation = 10× FCF = ~$375M EV

2026 valuation = ~6× FCF = ~$350M EV

Overall grade: 9/10

🎁 Bonus content

Sometimes we stumble across great little reports from the most unexpected corners of the market. But this time, the gem came from a company we already own.

We’d definitely recommend reading it. It’s a solid way to get a better feel for this beast of a business in the making.

🙏 Feel free to ❤️ and comment so that more people can discover and enjoy this Substack 😇

🔥🔥

May I ask. You predict 2025 revenue for Sanuwave to be over 100 million usd while the company itself is estimating only 50 million usd in revenue. How do you explain the difference? Also, don’t you think they’re giving discounts for large purchases or for convincing people to buy?