🧗 Our Investing Journey (#3): Investing, the Zero-Sum Game

Exploring the wisdom of crowds, subjective value and financial transactions

Hi buddy 👋

Welcome back to 🧙♂️ The Hermit 🧙♂️

ICYMI:

🧗 Our Investing Journey: Independent Thinking Abril 2024

📝 Company Updates: Cardlytics Dilution March 2024

If you haven’t yet, subscribe to get access to these posts, and every post

My Godfather

My godfather recently said that all investments are a zero-sum game. Personal experiences do lead to rules of thumb that ensure we avoid further pain from unpleasant situations. I’m naturally skeptical (and a bit of a nuisance) when people talk about rules applying to investing, so why not explore the topic?

My godfather is not a financial expert, but

a) he has lived long enough to understand the basics, and

b) he is naturally curious which pushes him to be a lifetime learner even as he reaches his 60s.

By training a medical doctor, this self-made man concluded that the entire game was zero-sum after a few fights in the real estate and pension fund arenas. In other words, he believes that for someone to win someone else must lose.

The Information Problem

I'm sure most people who have dealt with the markets have done so with little to no success. I don’t want to sound like a jerk but, to be honest, it’s mainly their fault. People jump into the markets thinking they can outsmart and outmaneuver the herd. The issue lies directly in the process as markets can rarely be outsmarted. The wisdom of the collective voting (buying/selling) of millions of individuals is rarely in the wrong.

This is especially true in the more popular arenas. Popular assets include as large companies (Apple, Meta, Google, Nvidia), city-center real estate, long-term government bonds (10+ yrs), commodities, and even mainstream cryptocurrencies (Bitcoin). All of these have in common a large number of interested parties and transaction volumes. As a result of the assets changing hands frequently, we have a more efficient price discovery.

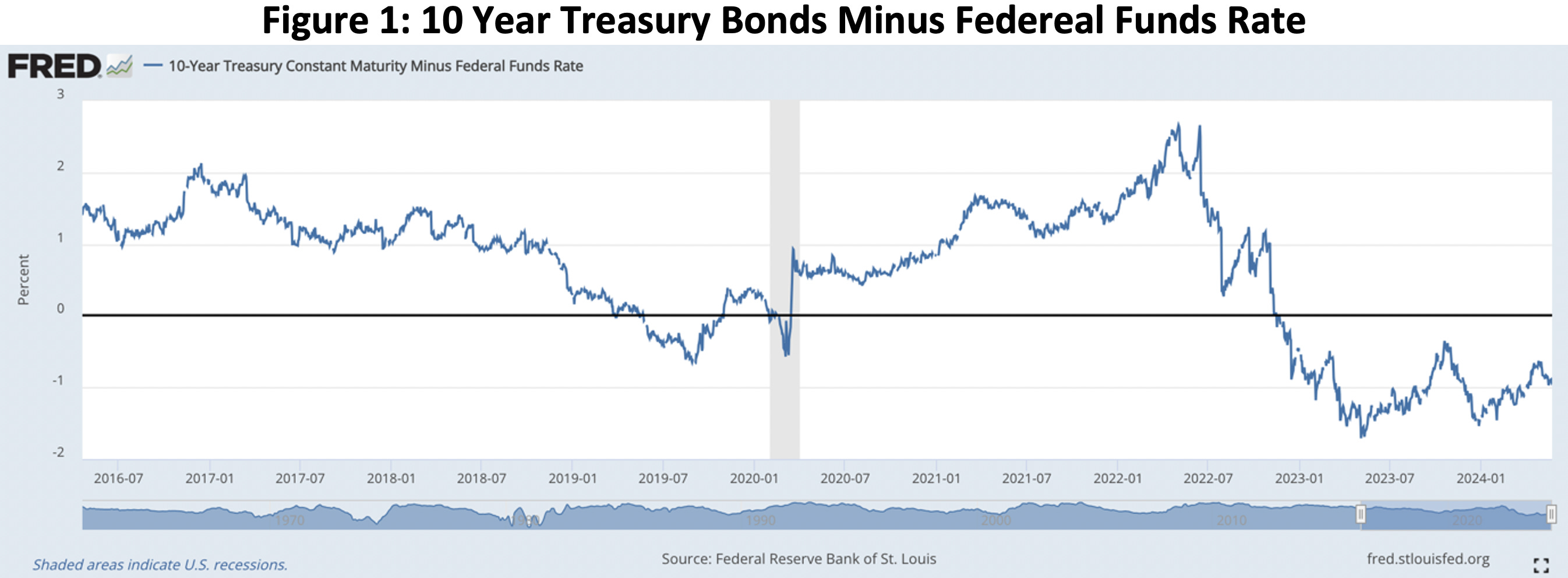

The wisdom of crowds is so powerful, that it can challenge the best groups of technocrats and specialists in any field. The prime example is the Federal Reserve rate vs the 10-year yield treasury. It does not matter how qualified the representatives of the Fed are as they cannot adjust the rate on a real-time basis by incorporating every piece of publicly available knowledge. But the markets can. That is why experts in the field use the 10-year treasury yield as the basis for the cost of capital, as it provides the most accurate measurement of the value of future money. Contrary to popular belief, I would argue that the Fed rate is but a lagging indicator of the 10-year rate.

Figure 1 portrays the difference between the market rate and the Fed rate. The market indicated rates should go up faster from the pandemic to late 2022. After this date, rates should have reversed. Small variations may not sound important, but they really are as they determine which projects are worth building and which are not. Especially after lagging the market by 2 percentage points, anyone can say that the Fed was late increasing rates. The point is rates have thousands of factors embedded into this one number, and the market can process them in real time with a minimal degree of error.

On the flip side, underfollowed assets can have egregious misvaluations for extended periods because of the lack of price discovery. Examples include companies with small market capitalization, low-quality bonds, real estate in small villages, and farmland. In general, undiscovered resources, may that be oil underground or a company spitting out hidden free cash flows, take intrepid explorers to uncover. The process of discovery takes additional steps in the form of spreading the word and accumulating interest for a fair price to form.

In the field of the undiscovered, you get both type 1 and type 2 errors frequently. Type one would equate to owning a piece of gold and people pricing it as a turd, and type two would be owning a turd and people pricing it as gold. The former are what one would call opportunities and the latter would be more of a scam.

Most people deal directly with these underfollowed assets and sadly have dealt with the “owning a turd and thinking it’s gold” situation. In this arena, a lack of critical judgment and an information asymmetry can lead to painful outcomes.

How many times have you acted on a stock tip? How many times have you seen people around you invest in a “risk-free project that will yield a 100x return”? The prime examples are casino games or the lottery where the probability-weighted outcome is, with a total degree of certainty, a turd.

We’ve all been there. The real sad part is not experiencing this event, but rather extrapolating this feeling into every other investment decision you make throughout your life.

The Zero-Sum Game

Within the voluminous financial landscape, players can encounter zero-sum games. For instance, an Over the Counter (OTC) product is a two-party transaction where, by definition, one player must lose so the other can win. These are commonly known as derivative contracts (forwards, warrants, swaps) that involve two parties that want to split risk. In most cases, the seller wants to reduce risk by setting in guaranteed profits and the buyer wants to take on risk to speculate on the underlying asset (usually because they think they can predict certain future events that will drive the price of an asset up or down). If people place this bet, one party will pay the other at a determined future time. One therefore has to lose for the other one to win.

But what if I told you, the game is not really zero-sum? Sure, one is forced to pay the other, but what if it was not all about the payment, but instead about the risk distribution? Here’s a quick example:

Let’s assume a farmer is considering planting a certain crop. The price of the crop is uncertain as whatever he plants today will be harvested after several months. For this reason, he pays a third party some money to buy a (forward) contract that will guarantee he can sell that crop at today’s market price (T1). He therefore locks in the profits as he knows the approximate crop yield (quantity) and costs he expects to incur. Once the crop is harvested at T2, the farmer will be forced to sell at the established price to a specified third party. Immediately the third party can turn to the market and sell that crop at market rate for a profit or a loss.

In the scenario described above, all parties win. However, when the market price is below the established fixed price, the speculator will lose. Even though, the risk bearer (speculator) loses, the overall transaction is a net gain as the entire point of the transaction is for the farmer to produce a good. If the farmer produces the crop, we get cereal, vegetables, legumes, rice, maize, nuts, soybeans, etc. When the farmer produces society profits.

The Value Cycle

If a person decides to go ahead with a transaction, it is because the exchange of goods and services nets them additional value. In other words, people transact their time for money and then transact money for goods because they perceive they are better off after the transaction. Let’s see this illustrated:

Before continuing with a brief explanation of the illustration above please take a moment to appreciate my impeccable artwork. Everyone can clearly tell that the 20-hour PowerPoint course has paid off ;D

Figure 4 is a depiction of the value generation of most transactions. Tim (appropriately named character) is willing to give Apple $100 for the newest iPhone because he knows that the iPhone will provide entertainment, utility, and productivity enhancements. This added value is represented by the x and is defined entirely by each individual. It is completely subjective but, nonetheless, the ultimate reason for carrying out the transaction. Apple on the other hand, can produce, market, and distribute the iPhone for $75 which means that, for every Tim who’s willing to pay $100 for an iPhone, they will make $25. Both transactions are a net positive individually AND a net positive for society.

Some added value can be quantified, like profits for a company, but most of the added value is perceived. This was proven by the eminent libertarian economist Ludvig von Mises in his theory of marginal utility. He stated that the value of consuming a water bottle when thirsty is much higher than the value of consuming a second bottle after you are done with the first. And the same is true for the third, fourth, etc. To the point where consuming too much can lead to negative value. In the case of water, if you drink more than 4 liters in a day, it can lead to overhydration.

Note that some transactions may not add value to your life, however, these are usually set up in extreme contexts, have hidden flaws, and/or lack explicit consent from one of the parties (involuntary transactions). Examples include exchanging a large sum of money in a kidnapping, buying a car that seems okay but has hidden issues, or paying taxes in exchange for… something (I guess).

An Average - Financial - Transaction

To sum it all up, we will now go through an average financial transaction. Let’s use the share price of Google for the last 5 years. The black line represents the approximate intrinsic value or real value of the underlying company.

Here’s what we know:

1. We know that customers of Google value the search engine and ad network (among many other things) that the company provides. So much so that the company makes large profits from servicing a huge customer base.

2. We know that the wisdom of crowds applies, as the company is well covered by both institutional and retail investors.

3. We also know that value is subjective and therefore two individuals might agree that they should buy the share. Nevertheless, one party can make much more optimistic assumptions, determine that the value is much higher, and thus be willing to pay a higher price than the other party.

4. Combining points 2 and 3. At times, the crowd can pull together and make very pessimistic or very optimistic assumptions for long periods of time. This leads to the shares being undervalued or overvalued with respect to their intrinsic value.

Let’s look at an example where Tim buys some shares. After a few months of hard work, Tim decides to pay $1,000 for 10 shares of GOOG 0.00%↑ in February 2023. Assuming there is only one counterparty and that there are no frictional costs, this means someone sold those shares at that same time for that same price. Presently, the price of the share is about $175 which means Tim killed it with a 75% in about 1.5 yrs. Tim clearly won, but can we say the other party lost? We cannot.

Assuming it’s not a meme stock, the only reason you would buy shares of a company is because you think that intrinsic/real value is higher than the current price.

However, people sell shares for many reasons. Sure, it can be because the person thinks that intrinsic value is lower than the current price, but it can also be because they found a better opportunity. It could be because they could not bear the volatility and would rather have more stable investments. It could be because their time horizon for the cash expanded, and therefore want a riskier investment. Or, on the contrary, their time horizon contracted and they needed the money for a family emergency. After all, I doubt you would consider selling Google and buying Nvidia in February 2023 a bad decision when Nvidia has returned 420% in the same period. Nor would you consider selling the shares to pay for your brother’s cancer treatment a loss.

In closing, most financial transactions have only winners because the uses and utility of money are subjective. There is only one reason for buying, but there are many reasons for selling. Rational actors work almost exclusively with opportunity cost known in financial lingo as the Weighted Average Cost of Capital (WACC), but that is a topic for another post.

Have a great rest of the week,

A. Yela