Atlas Engineered Products $AEP – Truss(t) the Process

Structurally Sound Fundamentals in a Canadian Consolidation Play

Investment Archive: Atlas Engineered Products ($AEP) The complete chronology of our research and primary data

Investment Thesis is our core series where we break down standout public companies so you understand exactly how they make money, where the risks lie, and why the opportunity exists long before the market agrees.

Most small-cap ideas are trades. This is a compounder.

In this deep dive, we break down one of our highest-conviction holdings, a company transforming a fragmented, manual industry into an automated money machine. The business is led by a rare combination: an engineer with a “war-time” operating mentality and a legendary capital allocator. Their strategy blends short-term competitive ferocity with long-term empire building.

This report is built on primary research, including exclusive commentary from the CEO and Director.

This content is intended for informational purposes only and should not be taken as investment advice. The author does not represent any third-party interest, and he may be a shareholder in the companies described in this series.

Please do your own research or consult with a professional advisor before making any financial decision. You will find a full disclaimer at the end of the post.

Context

The Business

Investment Case

🔍 Business Overview

Okay, Alejandro, I’ll give you a sense. When we build a house, we get maybe $5 a square foot for roof trusses. And roof trusses are 99 % of the wood frame industry uses a prefabricated roof truss like ours, 99%. The industry is saturated.

For (prefab) wall panels you get about $15 to as much as $20 per square foot. So every time you sell a house now, you can get three to four times the revenue you did before just with roof trusses. Now, prefabricated wall panels are probably 1 % of the industry right now. That’s how much adoption there is.

We think it’s gonna get to 50% within the next five years. So that industry alone is likely gonna have 50X in our mind. So when you talk about the opportunities that people don’t get it.

People don’t understand the opportunity set for this type of business. And what we’re finding is more and more of our customers are coming to us and saying:

“look, we don’t want to just buy roof trusses. We want to buy the whole package.”

So very few of our competitors are going to be anywhere in a position to able to deliver that. So that’s why we get so excited about this thing. Yes, it’s cyclical. Yes, it’s seasonal. Yes, lumber prices do this and that. But when we see what this thing looks like in five years, it is nowhere close to where we are right now.

We have not even started.

— Paul Andreola, director

Atlas Engineered Products is one of Canada’s leading manufacturers of engineered wood components, producing roof trusses, floor systems, wall panels, and other structural elements used in residential and light-commercial construction.

The sector is (to say the least) fragmented, dominated by small regional shops that rely on manual processes, aging equipment, and limited purchasing power.

AEP’s strategy is to modernize this landscape through a very disciplined consolidation and automation model.

They acquire these smaller operators at attractive valuations, upgrade their equipment, implement standardized engineering software, streamline production flows, and centralize procurement.

This creates a structural cost advantage that makes AEP one of (if not) the lowest-cost producers in a commodity-driven market where price and reliability determine who survives.

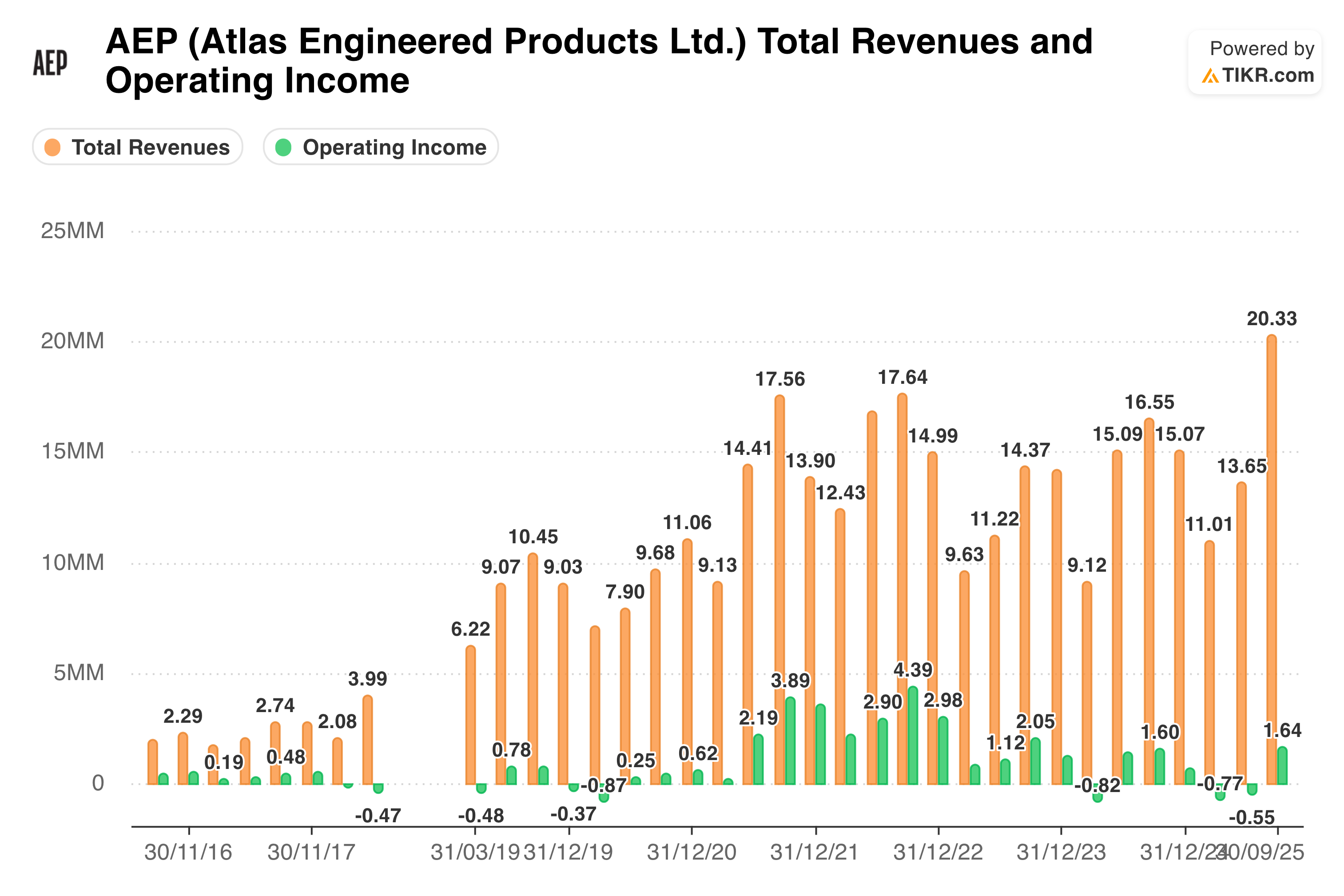

Here’s a quick financial review. In 2024, AEP generated C$55.8m in revenue, a 13% YoY increase, with standout growth in Wall Panels (+159% yoy) and Engineered Wood Products (+21% yoy). EBIT was about C$2.90m (5% margin, down from 20% in 2022), including C$645k in automation and expansion costs.

As of mid-2025, the company reported C$24.66m in revenue and an operating loss of C$1.32m for the first six months, with materials, labor, and overhead accounting for most of the cost base.

More interestingly, the company reported a record revenue quarter yesterday (helped by overdue backlog from Q2), delivering C$20.33m in revenue and C$1.64m in EBIT.

Long-term debt stands at roughly C$19.40m, with net debt around C$16.30m. With a market capitalization near C$45.66m and an EV/Sales multiple near 1.0x, the market still prices AEP as a small, cyclical operator despite its growing scale and improving efficiency.

Growth continues to be driven by acquisitions. Recent deals, such as Truss-Worthy Construction Systems in Ontario (C$1.58m plus real estate) and Penn-Truss MFG in Saskatchewan (C$3.8m), expand both geographic reach and operational density. We’ll look at all the transactions in great detail later.

Each acquisition strengthens AEP’s flywheel of increased design capacity, higher procurement leverage, standardized processes, and improved logistics across its network. This integration model is the core of their competitive edge. As they expand, AEP becomes increasingly difficult to outprice, especially in an industry where structural components behave like commodities and buyers favor the lowest cost that meets quality standards.

AEP’s methodology drags an outdated manufacturing niche into the 21st century, transforming it into the competitive machine it needs to be, and delivering a product that’s 10x better within the same old business of house building.

Another simple thing to understand, so the way homes are being built right now, when you frame a house, it can take up to six weeks on average for a single family house to be completely framed. When you prefabricate the components, walls and floors and roofs, you can get it installed in three days.

So it goes from six weeks to three days.

So when you’re a builder and you’re going through a lot of homes, that not only are you getting built faster, but you’re actually getting paid much faster.

So these contractors need to move their cash as fast they can. So that’s why there’s more adoption of all this prefabrication. It just speeds up the process.

— Paul Andreola, director

Trade dynamics reinforce their position. About 25% of US-consumed lumber comes from Canada, and tariff cycles (*cough* Trump-era duties *cough*) can distort pricing in ways that reward efficient producers.

In boom cycles, AEP’s cost structure expands margins; in downturns, weaker competitors face losses or exit the market, creating further acquisition opportunities.

The company effectively benefits from both ends of the macro cycle.