Crocs Inc. $CROX – Clogging Up the Bank

Buybacks, Deleveraging, and Hidden Earnings Yield of the Polarizing Ugly Shoe Giant

Investment Archive: Crocs Inc. ($CROX) The complete chronology of our research and primary data

Investment Thesis is our core series where we break down standout public companies so you understand exactly how they make money, where the risks lie, and why the opportunity exists long before the market agrees.

Yeah, yeah… I know guys. You’ve been wanting this for a long time, and at the current price…

It’s a no-brainer.

Thanks to a partnership with Stripe, we’re able to keep the core of this deep dive open and free for everyone today. So please enjoy.

Inside the growth engine of AI’s breakout companies

Companies like ElevenLabs, Runway, and Leonardo AI maintain rapid growth while others stall on complexity.

As businesses grow, payments break, billing gets messy, and engineers stop building to fight fires. Stripe’s playbook reveals how these leaders built infrastructure that scales.

This content is intended for informational purposes only and should not be taken as investment advice. The author does not represent any third-party interest, and he may be a shareholder in the companies described in this series.

Please do your own research or consult with a professional advisor before making any financial decision. You will find a full disclaimer at the end of the post.

Context

The Business

Investment Case

🔍 Business Overview

Crocs ($CROX) was and is a company that produces what is essentially a piece of Swiss cheese for your feet. It is the ‘cilantro’ of footwear, you either love it with a cult-like devotion or you think it’s a genetic mistake that should never have occurred in nature.

Regardless of your fashion soul, preferences, and whatnot, the business itself is a masterclass in high-margin absurdity.

At its core, Crocs doesn’t really sell shoes, instead they sell their tech Croslite. And you may ask yourself, what is that?

It’s their tech… their proprietary, closed-cell resin that is neither plastic nor rubber. It’s light, it’s odor-resistant, and most importantly, it’s incredibly cheap to manufacture (especially in Southeast Asia).

While competitors are fumbling with leather uppers and complex stitching, Crocs basically pours ‘magic goo’ into a mold, waits a few minutes, and pops out a 60% gross margin product.

The real genius (and one of their latest updates), however, is the Jibbitz, those tiny plastic charms you shove into the holes of the clogs.

The strategy is pretty simple: they sell you a ‘holed’ shoe and then charge you $5 bucks a pop to fill those holes (hopefully this will sound professional in your mind).

It is kind of the ultimate ‘DLC’ (Downloadable Content) of the physical world.

The margins on Jibbitz are rumored to be so high they’d make a software executive blush. Sadly, they don’t really disclose these, but know it turns a commodity shoe into a personalized billboard, creating a stickiness that keeps Gen Z, kids, and healthcare workers coming back for more (essentially every year).

In 2022, Crocs decided they needed MORE… and dropped $2.5bn on HEYDUDE a brand that makes lightweight loafers for people who find Crocs too extravagant.

On paper, it was already iffy; we would’ve paid about 20% of the amount mentioned above for it, but they probably saw some synergies that we don’t, which made it overall very compelling for them at the time.

In practice, we will note that the integration we’ve seen has only led to a mounting pile of issues.

That’s why it’s currently undergoing a massive brand surgery, clearing out gray market inventory and trying to prove it wasn’t just a pandemic-era fluke. If they fix it, the company becomes a multi-brand powerhouse; if they don’t, it’s a very expensive (M&A) lesson .

Going back to basics, Crocs has achieved a rare thing in our fast fashion, which we will call it: Strategic Polarisation.

By being unapologetically ‘ugly,’ they’ve built a moat that traditional brands like Nike or Adidas can’t touch.

Why?

Because those brands have to be ‘cool’.

Crocs just has to be Crocs.

They’ve leaned into the ‘so bad it’s good’ vibe through collaborations with everyone from Post Malone to Lightning McQueen, turning a gardening shoe into a high fashion statement.

Crocs are the ultimate “I’ve given up, but I’m winning’ footwear.” They are functionally indestructible, emotionally confusing, and financially a fortress.

Why does this matter to us?

Because underneath the memes and the foam lies a business with Ferrari-level margins plus a suite of financial engineering through debt repayments and share buybacks that is working overtime.

Usually, we’re hunting for the rare gems in the $50m–$100m market cap range. This pick is a massive outlier for us, but we’re stepping out of our typical lane for a very good reason.

Even though this is a global, highly professionalized business, quite a far cry from our usual scrappy micro-caps, we didn’t change our play. We applied the exact same scuttlebutt approach, digging into the primary data and ground-level reality rather than just skimming polished investor decks.

This report features direct commentary from:

Abigail Ritter, Investor Relations

Emily Nutting, Investor Relations

And it, of course, contains insights from a few dozen professionals ranging from podologists to large-scale users.

In this deep dive, we’re peeling back the foam to see exactly why Crocs is such a high-conviction play right now. We’re moving past the ugly shoe memes to look at a business with a structural moat as wide as its toe box, and more importantly, we’ll answer the big questions: ‘What Is It?’, ‘Why now?’, and ‘How Much?’

Speaking of memes… I thought this was (contemporarily) absolutely fantastic:

🌱 Origin Story

Every great company has a founding myth, and the story of Crocs doesn’t start in a corporate boardroom but on a boat in the Caribbean in the spring of 2002.

Three friends from Colorado, Scott Seamans, Lyndon ‘Duke’ Hanson, and George Boedecker Jr. were sailing when Seamans pulled out a pair of foam clogs he had found from a Canadian manufacturer called Foam Creations.

The shoes were technically hideous, bright green, full of holes, and looked like something you would use to hose down a boat deck. But on the wet, slippery surface of a boat, they were a revelation because they were slip-resistant, they floated, and they were absurdly comfortable.

The founders realized that while the world might see an ‘ugly’ shoe, boaters would see a vital tool.

They bought the rights to the proprietary material, which they later branded as Croslite, and improved the design by adding the now iconic heel strap.

They officially unveiled the product at the 2002 Fort Lauderdale Boat Show with just 200 pairs. They sold every single pair immediately, not because of a fashion trend, but because people who spend all day on their feet recognized a ‘sweet spot’ in the market for functional comfort.

They named the company Crocs because the profile of the shoe looked like a crocodile snout and, much like the animal, it was designed to perform perfectly on both land and water.

The early 2000s were a rocket ship for the brand as it transitioned from a practical tool for boaters to the unofficial uniform of healthcare workers and chefs who valued the slip-resistant Croslite material during long shifts.

Quick pause. You’re going to like the story of Jibbitz.

They weren’t invented by the Crocs founders, but by a stay-at-home mom named Sheri Schmelzer in 2005. She was literally just tinkering in her basement with her kids, using clay and rhinestones to plug the holes in their shoes to make them look cuter.

Her husband, Rich, saw the potential, and they launched a website in August 2005. It blew up so fast that by 2006, Crocs realized these tiny pieces of plastic were their secret weapon for personalization and bought the whole company for $10m (plus another $10m in earn-outs).

It turned out to be one of the best acquisitions in retail history.

Plastic flair!

Let’s keep going with Crocs.

By 2006, the company went public in one of the largest footwear IPOs at the time, with its stock price soaring from $21 to $75 in less than a year.

By 2007, the brand was moving 130,000 pairs every single day, proving that sometimes the best business strategy is simply solving a problem with ‘magic goo’ and a bit of sailing intuition.

But the higher the climb, the harder the fall.

In 2008, the company was staring down a bankruptcy barrel. They had overexpanded recklessly, warehouses were overflowing with unsold inventory, and the Great Recession hit consumer spending like a freight train. The stock price that was once $75 plummeted to below $1, and Crocs became a Wall Street meme name often compared to a zombie company.

The turnaround didn’t happen overnight. It started with a $200m investment from Blackstone in 2013 and truly hit its stride when Andrew Rees took over as CEO in 2017. Rees made the brave call to stop pretending the shoes were pretty. Instead, he embraced the ‘ugly’ aesthetic as a badge of honor and consolidated the product lines to focus on the core clog that everyone loved to hate.

Ever since, they’ve launched cultural counterstrikes through collaborations with high fashion giants like Balenciaga and superstars like Post Malone and Justin Bieber, turning a gardening shoe into a limited edition fashion weapon.

In 2022, they made a massive $2.5bn bet by acquiring HEYDUDE to diversify their portfolio beyond the foam clog. They’re still working on the consolidation as of April 1st 2026.

🌐 Industry Overview and Competitive Landscape

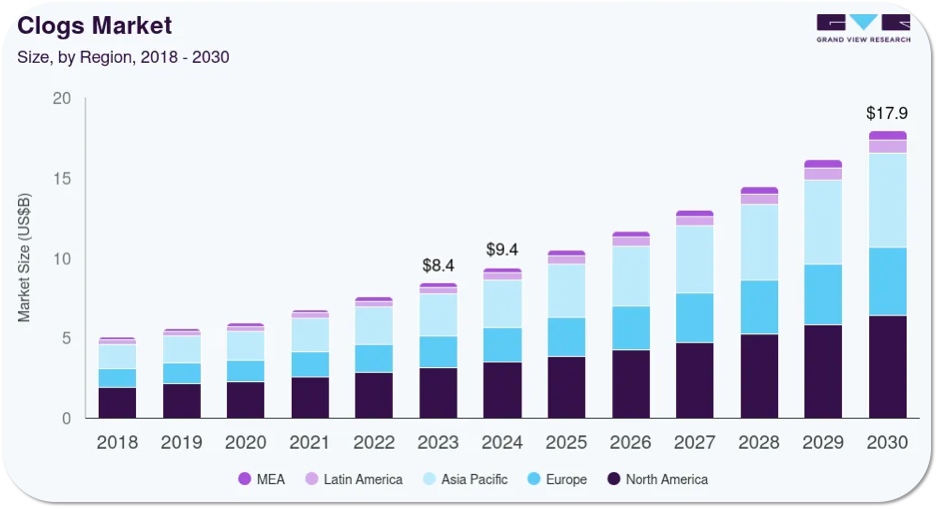

Crocs operates in the massive $160bn casual footwear market. Within this world, they dominate the $15bn clog niche but are also aggressively carving out space in the $35bn sandals category.

While the market likes to lump them in with athletic giants like Nike or Adidas, that is actually a mistake. Crocs does not compete for the ‘performance running’ dollar. They compete for the ‘casual comfort’ dollar.

A Few Key Players

The competitive landscape is defined by a few key players:

Deckers Outdoor is the closest rival, owning UGG and HOKA. Like Crocs, Deckers relies on ‘ugly cool’ silhouettes and extreme comfort. However, Wall Street treats them very differently.

Deckers often trades at a significant premium because of HOKA’s growth, while Crocs trades at a fraction of that multiple despite having similar operating margins.

Birkenstock is the premium player in the room. They play a ‘premium accessible’ game with a 250 year history, but their production is complex and expensive. Crocs has a simpler, more scalable injection molding process that allows for much better agility and higher margins.

Skechers dominates the mass market affordable sector. They compete on volume and price rather than hype, but they operate with much lower gross margins than Crocs. While Skechers hits around 45-50%, Crocs consistently clears 55-60% because of its brand power and proprietary material.

The irrationality of the current market is best seen in the valuation gap. While competitors like On Holding trade at sky-high multiples above 50x PE (30x forward PE), Crocs is currently sitting in the single digits.

With a clean balance sheet, an international business ripping at a 30%+ clip, and free cash flow margins sitting north of 16% (currently 19%), the company is starting to look like absolute candy for anyone hunting for quality at a discount.

Among value investors, the consensus is that the market is applying a ‘fad discount’ to a brand that has already proven its durability over two decades.

Crocs is the lowest cost producer in a high demand category with a moat built on strategic polarization.

🧩 Business Model

To understand how a foam shoe company generates luxury-level margins, you have to look at the machinery behind the brand.

Crocs operates a business model that is fundamentally different from traditional footwear giants like Nike or Adidas. It is less of a shoe manufacturer and more of a high-efficiency marketing and distribution engine.

Q: I want to know about you prioritizing these buybacks versus paying down debt versus investing in the Hey Dude brand as in like CapEx, new CapEx. What’s the framing for this?

IR: First and foremost is reinvest in the brand. That’s primarily going to be in software, IT infrastructure, as well as direct to consumer investments.

The second would be to remain within our one to one and a half times that leverage that is anchored by debt covenant related to our TLB (loan terms) of two and a half times that leverage.

We will redeploy all that excess free cash that we generate because we do generate a lot towards share repurchase. Clearly we are over indexing to share repo given how we view our shares internally.

Unit Economics and Manufacturing

The foundation of this business is a proprietary platform consisting of a unique material, a radically simplified manufacturing process, and a highly agile, asset-light distribution network.

At its center is Croslite, a proprietary closed-cell resin technically known as a Proprietary Closed Cell Resin or PCCR.

This material is a distinct compound that reacts to body heat, allowing the footbed to conform to the specific shape of the wearer for a custom fit. Because it is non-porous, it does not absorb sweat, water, or bacteria, making the shoes naturally odor-resistant and easy to sanitize.

To protect its moat against environmental criticism, the company began integrating biocircular Croslite in 2021, which incorporates bio waste and industry byproducts like used cooking oil to reduce the carbon footprint of its classic clog.

Utilizing a single-piece injection molding process that is fundamentally different from the additive and labor-intensive assembly lines used by traditional footwear giants.

While a typical sneaker can require over 40 separate parts to be stitched or glued together, a classic clog is popped out of a single mold in a matter of minutes.

This efficiency creates a zero-waste loop where production scraps are reground into pellets and fed back into the machinery, with roughly 7.3% of the material in their 2023 portfolio coming directly from their own recycled waste.

This simplified process also grants a massive lead time advantage, allowing the brand to move from a new color or collaboration concept to a finished product in weeks rather than the six to nine months typical for competitors.

This simplicity translates directly into an industry-leading financial profile, with gross margins consistently hovering between 55% and 60%.

The business operates on an asset-light model, outsourcing 100% of its production to third-party partners primarily in Vietnam, Indonesia, and China.

This model provides incredible scalability and geopolitical agility, as the company can shift production volumes between regions relatively quickly because the mold and resin setup is highly portable compared to a complex stitching factory.

Just like Coke’s formula, the Croslite foundation allows the company to operate with a premium status at a worldwide stage.

Ecosystem: Clogs, Sandals, and Jibbitz

The revenue engine is split into three main pillars.

The Classic Clog serves as the undisputed cash engine of the brand, generating roughly 75% of total sales and functioning as a ‘tollbooth’ product that creates a stable floor of recurring demand.

Unlike high fashion trends that flame out, the clog is anchored in the functional needs of essential workers like nurses and chefs, alongside a massive student demographic that prizes utility and ease. More on this later.

This creates a defensive layer to the business; even when general consumer spending tightens, the need for comfortable slip-resistant work footwear provides a predictable revenue stream that management can rely on to fund more aggressive growth initiatives.

Because the product has essentially remained unchanged for two decades, the company avoids the heavy R&D and fashion risk associated with constant redesigns, allowing the clog to act as a pure margin harvester that subsidizes the rest of the portfolio.

Expanding beyond the clog, the company is aggressively targeting the $35bn global sandals market, which currently represents about 13% of brand revenue but serves as a critical bridge to new wearing occasions.

This is a strategic low-friction extension because it utilizes the same proprietary Croslite technology and manufacturing molds while appealing to consumers who might find the traditional clog silhouette too polarizing for every situation.

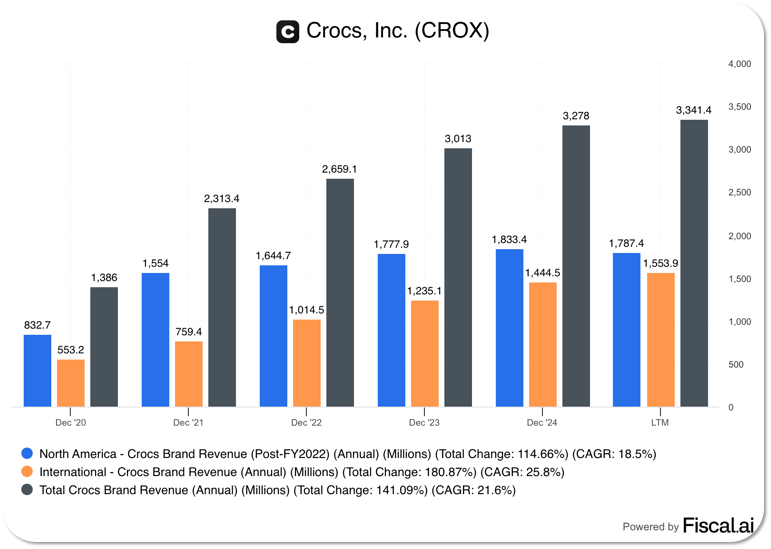

This expansion is particularly vital in international markets where sandals often have a higher penetration rate than the classic clog, providing a clear runway for the 39% CAGR seen in international growth since 2020.

Perhaps the most brilliant element of the financial model is the Jibbitz business, which accounts for approximately 8% of sales.

While the top-line contribution seems modest, the economic impact is outsized because these charms carry estimated margins north of 80%, significantly lifting the overall blended margin of a transaction.

Prices [key]

The pricing journey for Crocs started as a functional $30 boat shoe in 2002 and stayed in the $30-35 range for nearly a decade while the company focused on volume and global reach.

Things changed significantly when Andrew Rees took over as CEO in 2017 and realized the brand had the cultural permission to move up the value chain.

He strategically raised the MSRP of the Classic Clog to its current $50 level, which provided a massive boost to the bottom line without scaring off the core customer.

This move was supported by a ‘collaboration playbook’ in which limited-edition pairs with luxury houses or celebrities retail for anywhere from $75 to as high as $850.

This strategy allows the company to maintain its ‘everyman’ image while capturing high-margin collectors’ willingness to pay.

By keeping the entry price of the shoe relatively accessible, the company encourages customers to spend an extra $20-30 on personalization through Jibbitz charms and customization packs, effectively doubling the profit per transaction.

Note that the portfolio has expanded to include sandals and slides priced between $30-40 to capture more ‘wearing’ occasions, while the HEYDUDE brand is positioned at a slightly higher $60 price point.

HEYDUDE is currently in the bargain bin phase as management uses markdown support to flush out old inventory from wholesalers.

In contrast, the core Crocs brand is a fortress. It has stubbornly held its $50 price point even while inflation and a shaky economy forced most of the retail sector to slash prices just to stay afloat.

They won’t hike prices with inflation, but simultaneously won’t discount in times of need. As Investor Relations says…

Crocs is a want brand.

Asset Light Distribution

The company has mastered a sophisticated hybrid distribution model that perfectly balances the massive reach of traditional retail with the high-octane margins of digital commerce.

By maintaining a roughly 50/50 split between wholesale and direct-to-consumer (DTC) channels, they have created a ‘volume engine’ through partners like Journeys and Foot Locker that ensures the brand is visible in every major mall in America.

This wholesale presence acts as a massive billboard, but the real magic happens in the DTC segment, where the company sells directly through its own websites and high-growth platforms like Amazon.

By cutting out the middleman on half of their sales, Crocs captures the full retail price, which creates a structural expansion in operating margins that most footwear competitors simply cannot match.

This digital-first pivot has transformed the brand into a social commerce powerhouse, famously reaching the number one spot on TikTok Shop for footwear.

This is a fundamental shift in how the business operates. By leveraging viral social trends and direct sales funnels, management has been able to quadruple sales in just five years while simultaneously slashing SG&A expenses from over 47% to under 30%.

They are essentially running a high-performance tech playbook on a physical product, using data from their digital storefronts to understand exactly which ‘drops’ or Jibbitz designs will move the needle before they even hit the warehouse.

The financial beauty of this setup lies in its asset-light nature. Because Crocs outsources 100% of its production to third-party manufacturers, they avoid the heavy capital trap of owning and maintaining massive factories.

Instead, they can funnel their massive free cash flow into high-return areas like IT infrastructure, global logistics, and buybacks.

This distribution strategy allows them to remain incredibly agile, scaling up digital inventory when a collaboration goes viral or throttling back wholesale shipments to clean up ‘gray market’ inventory, as they are currently doing with the HEYDUDE brand.

Personalization and Collabs

The company has essentially pioneered a physical version of the ‘DLC’ or ‘downloadable content’ model typically seen in the software industry.

By designing a shoe with exactly 13 holes per foot, they are selling a recurring subscription to self-expression. Each of those holes represents an invitation to purchase a Jibbitz charm, which usually retails for around $5.00 but costs only a fraction of that to produce (probably around $1.00).

This add-on strategy creates a psychological lock-in where the customer becomes the co-designer of the product.

It turns a mass-produced commodity into a personalized item, ensuring that no two pairs in a high school hallway or hospital ward look the same. This personalization loop is a key driver of the brand’s stickiness, particularly among younger demographics who value individuality over traditional brand uniformity.

… And all of it without the heavy R&D costs associated with traditional footwear innovation.

While a brand like Nike might have to engineer a new Air sole or complex knit pattern to stay relevant, Crocs simply treats its classic clog as a blank canvas for high-frequency collaborations.

Their partnership playbook is incredibly broad, ranging from high fashion houses like Balenciaga and Simone Rocha to global superstars like Justin Bieber and Post Malone, and even reaching into the ‘absurdist’ realm with brands like KFC or Pringles.

These partnerships operate on a scarcity model, using limited edition drops to create a sense of urgency and hype that keeps the brand perpetually in the social media conversation.

By utilizing the same injection molding process but swapping out colors, resins, and exclusive Jibbitz, they can react to viral trends with a speed that traditional manufacturers cannot match.

By partnering with icons who embrace the unconventional, they have turned the shoe into a badge of honor for those who prioritize comfort and authenticity over traditional ‘cool’.

Plus, the data gathered from these digital drops and social interactions allows management to understand consumer demand in real time, reducing inventory risk and ensuring that the most popular designs are always in stock.

Their product wear ranges from the ‘high fashion’ runway to the grocery store.

It really is a masterclass in using pattern interrupts to remain a fixture in the public consciousness, proving that in the modern retail landscape, being the subject of debate is just as valuable as being the subject of desire.

All publicity is good publicity.

Customers

Q: When it comes to core customer, there seems to be two massive groups which are caretakers and children, particularly people at school who buy a lot of these shoes. And I would love to know how you see the synergies between sort of the existing marketplace for Crocs and,when it comes to the Hey Dude brand, whether there’s any cross-selling that you can do, whether you’re applying any strategy on that end, particularly on the kid side. I’d love to know if you’re doing anything on that front.

IR: So we, a couple things. So we don’t break out the size of our kids’ business. The last time we did was many years ago and it was approximately 20%.

When we look at our brand, actually for both brands, we are an adult shoe company and the kids’ innovation is purely take downs of adult innovation.

So we say, let’s create X, Y, and Z products and then we’ll iterate on a couple of those for kids heading into the next season. I would say when the other piece that is a nuance is that we compete for wearing occasions, we are a want, not a need brand.

To understand who is actually putting these foam clogs on their feet, you have to look at the brand as a collection of high conviction tribes rather than a single mass market audience.

The most resilient pillar of the business is the essential workforce, specifically healthcare professionals and hospitality workers who treat the classic clog as a critical piece of equipment rather than a fashion choice.

For nurses and chefs, the appeal is entirely functional: the shoes are slip-resistant, they are lightweight enough for 12-hour shifts, and because Croslite is a non-porous resin, they can be bleached or hosed down after a messy shift.

This tollbooth group provides the structural floor for the company’s revenue because their demand is based on utility and replacement cycles rather than the whims of the fashion cycle.

Directly adjacent to the utility base is the Gen Z and Alpha demographic, which has transformed Crocs into a social commerce powerhouse.

This group is more interested in buying a blank canvas for self-expression.

The brand’s dominance on platforms like TikTok Shop (where it has previously held the #1 spot for footwear) is driven by the psychological sticky factor of Jibbitz.

For these younger consumers, the shoe is a physical version of a video game avatar that can be customized with charms to signal their interests, from favorite snacks to pop culture icons.

This has turned the brand into a high-frequency, low-ticket purchase category where kids and teens return (every year) to the store for both a new pair of shoes and their high-margin add-ons that keep their look current.

Geographical Diversification

While the United States remains the historical fortress for the brand, the current investment thesis is increasingly being written in foreign languages as management pivots to an aggressive international expansion strategy.

For years, the market viewed the company as a purely Western phenomenon, but the data now shows an incredible 39% CAGR in international growth since 2020, proving that the ‘ugly comfort’ value proposition translates globally.

This shift is a critical hedge against a cooling US consumer sentiment, where the middle class is currently under significant pressure and North American sales have shown signs of deceleration.

The most significant alpha in the geographic story is the massive momentum in China, which has become the blueprint for how the brand can conquer new markets.

By moving away from a one-size-fits-all approach, the company has utilized a ‘Korean Model’ of success, treating footwear as a high-fashion accessory through localized celebrity endorsements and a heavy focus on the digital ecosystem of Tmall and Douyin.

This Asian expansion is fueled by the realization that in many of these markets, sandals have a higher natural penetration than clogs, allowing the company to lead with its sandal portfolio to gain a foothold before introducing the more polarizing classic clog.

This geographic diversification is effectively turning the company from a US retail story into a global consumer staple play.

The European market, specifically France and the UK, has shown surprising resilience as the brand leans into its anti-fashion identity to capture a younger, more rebellious consumer base.

By spreading its revenue base across 80 countries, the company is no longer at the mercy of a single economy’s health.

This global footprint allows management to maintain high double-digit growth in international segments even as they deliberately slow down production in the US to clean up inventory and protect long-term brand health.

Doctors’ Assessment

Doctors are the brand’s biggest contradiction. We talked to more than a dozen and, surprisingly, there was a consensus in their verdict.

They wear them religiously for the easy-to-clean hygiene and 12-hour shift comfort, but they rarely prescribe them for everyday life.

Podiatrists point to one major mechanical flaw: the lack of a secure heel.

When a shoe is backless, your foot has to work overtime. Your toes claw at the footbed to keep the shoe from flying off, which can lead to hammer toes, tendonitis, and localized calluses.

It is great for a surgeon standing still for hours, but often problematic for someone walking long distances.

For children, the medical verdict is even more aggressive.

Kids have developing feet that are essentially soft cartilage looking for a mold, and they need structure to guide their gait. The wide, unstable toe box and lack of arch support in a standard clog can lead to gait issues and an increase in ‘trip and fall’ accidents.

Most podologists recommend that kids only wear them for short bursts, like the beach or the backyard, rather than as a primary school shoe.

While the brand has secured the ‘seal of acceptance’ from the American Podiatric Medical Association for some models, this is typically for specialized ‘RX’ versions designed for diabetics or people with massive foot swelling who need the extra volume and antimicrobial resin.

If you are using them as a recovery slipper after a long run or a cleanable work boot, you are using the product correctly. If you are making them a child’s primary footwear, you are likely ignoring the risk of long-term structural damage to the foot.

👥 Management

The current executive leadership team at Crocs is built around a mix of long-time veterans and new talent brought in from major competitors like Nike and Adidas.

Andrew Rees – CEO

Rees is the architect of the brand’s modern success. He joined the company in 2014 and became CEO in 2017, focusing the business on the classic clog and high-margin digital sales.

Patraic Reagan – CFO

Reagan joined Crocs in late 2025. He is a 14-year veteran of Nike and is currently tasked with managing the company’s cost-saving initiatives and the financial strategy for the HEYDUDE recovery.

Anne Mehlman – President (Crocs Brand)

Formerly the company’s CFO, Mehlman was promoted to lead the core Crocs brand in 2024. She oversees the global product and marketing strategy for the namesake clogs and sandals.

Rupert Campbell – President (HEYDUDE Brand)

Campbell joined in 2025 after serving as the President of Adidas North America. He was specifically brought in to lead the brand health surgery for HEYDUDE and stabilize its wholesale and commercial strategy.

Terence Reilly – Chief Brand Officer

Reilly is a highly regarded marketing executive who returned to the company after a successful stint as the President of Stanley. He oversees the global brand image for both Crocs and HEYDUDE.

As an extra note, you should look at the Stanley Cup rebranding engineered by this gentleman, here’s a video summary.

👞 HEYDUDE Integration

Q: Can you expand a bit on why you stopped or didn't bet that hard on the marketing and the things? What went wrong and how are you fixing that if you are?

IR: At the highest level, we shared that Hey Dude would be a billion dollar brand by 2024. Clearly not a billion dollar brand, right? So our cost base that's associated with Hey Dude continued to increase as if it was going to be a billion dollars in revenue.

It's not that.

So we have been right sizing really where we're spending across talent, across marketing, across overall distribution and logistics like really right sizing the cost base to match the business as it stands today.

What we have seen is that the actual ROI that we're receiving on performance marketing when it's not reaching there, we can quickly turn that spigot down and redeploy those dollars into brand marketing.

In December 2021, Crocs made its most aggressive strategic move to date by announcing the acquisition of HEYDUDE for $2.5bn.

The transaction was structured with $2.05bn in cash and $450m in shares issued to the brand’s founder, Alessandro Rosano, effectively loading the company’s balance sheet with a $2bn Term Loan B to fund the deal.

At the time, the rationale was seductive: HEYDUDE was a high growth, high margin business that perfectly complemented the Crocs DNA of clunky comfort.

It offered a massive foothold in the heartland of America with its lightweight Wally and Wendy silhouettes, providing a diversified revenue stream that wasn’t solely dependent on the foam clog.

Management initially projected that HEYDUDE would become a billion-dollar brand by 2024, a target that ultimately led to the integration’s biggest headaches.

The post acquisition honeymoon ended abruptly as the company realized they had inherited a business that grew too fast through undisciplined wholesale channels.

Q: I’m just pushing on the synergies between the two brands. I’ve interviewed a ton of people from pathologists to like teachers, preschool teachers and stuff like that.

And you either love or hate the Crocs brand. I can’t seem to find the same thing for the Hey Dude brand.

IR: It is absolutely polarizing when we look at our consumer base. The Wally Wendy is exactly the same. What I would say is like the heartland of America. That is the heartland of Hey Dude. The coasts do not like the brand, right? Or they don’t like the silhouette of that Wally Wendy. They find it polarizing. They don’t think it’s for them.

By mid 2024, the brand was facing a massive inventory glut, as gray market sellers flooded the internet with discounted products, severely damaging the brand’s pricing power and prestige.

This led to what management now calls brand health surgery.

In one of our interviews with investor relations, it was revealed that the cost base for HEYDUDE had continued to increase as if it were already a billion-dollar business, forcing the company to begin right-sizing everything from talent to marketing spend.

This culminated in a massive non-cash impairment charge in Q2 2025 totaling $737m, $430m for the trademark and $307m for goodwill, signaling to the market that Crocs had officially overpaid for the initial vision.

The integration strategy has since shifted from growth at all costs to a disciplined cleanup phase. The company is currently closing over 600 small, mostly unproductive (certainly uneconomical) wholesale accounts and performing a massive inventory take back to stabilize the channel.

As noted in the scuttlebutt research, this move is negative revenue (and margin) in the short term, but it is necessary to clear out the legacy socks program and female products that weren’t moving.

Management is now pivoting HEYDUDE away from performance marketing and back toward brand building, a strategy led by a newly assembled A-Team of industry veterans.

This includes Rupert Campbell, the former President of Adidas North America, and Patraic Reagan, a 14-year Nike veteran who was brought in as CFO to navigate the $150m in cost savings planned through 2026.

By the end of 2025, the company reported that wholesale was sequentially improving as they moved from absolute inventory take-backs to simple markdown dollar support for retailers.

The goal is to reach a long-term operating margin of 24-25% for the brand by 2026, anchored by a leaner distribution model and a heavy focus on direct to consumer (DTC) sales.

💵 Comprehensible Financials

As always, we’ll keep this part simple. We look for five core traits in every company we own:

Sensible leverage. Healthy debt levels and smart, disciplined use of it

Profitable growth. Steady revenue expansion supported by strong margins

High returns on capital. Efficient use of every dollar invested or employed

Cash discipline. Capital requirements and consistent free cash flow

Shareholder alignment. Minimal dilution and thoughtful per-share allocation