Computer Modelling Group $CMG – Dirt, Data, and Roper

Merging Niche Critical Software, Ultra Smart Capital Allocation, and Constellation Software Key Staff

Investment Archive: Computer Modelling Group Ltd. ($CMG) The complete chronology of our research and primary data

Investment Thesis is our core series where we break down standout public companies so you understand exactly how they make money, where the risks lie, and why the opportunity exists long before the market agrees.

This content is intended for informational purposes only and should not be taken as investment advice. The author does not represent any third-party interest, and he may be a shareholder in the companies described in this series.

Please do your own research or consult with a professional advisor before making any financial decision. You will find a full disclaimer at the end of the post.

Context

The Business

Investment Case

🔍 Business Overview

Imagine taking a legacy software monopoly, injecting it with the capital allocation DNA of Constellation Software, and letting it loose on the oil patch.

Introducing youuuur heavy oil chaaaaaaaampion of the woooooooorld…

Computer Modelling Group ($CMG)

Historically, this company has been a publicly traded university research department… chasing cool scientific anomalies instead of tangible commercial returns $$$.

But a recent pivot has turned this quiet Canadian cash cow into a weaponized software rollup engine.

If you appreciate capital discipline, negative working capital, and asymmetric tech bets, this is a business you can’t afford to ignore.

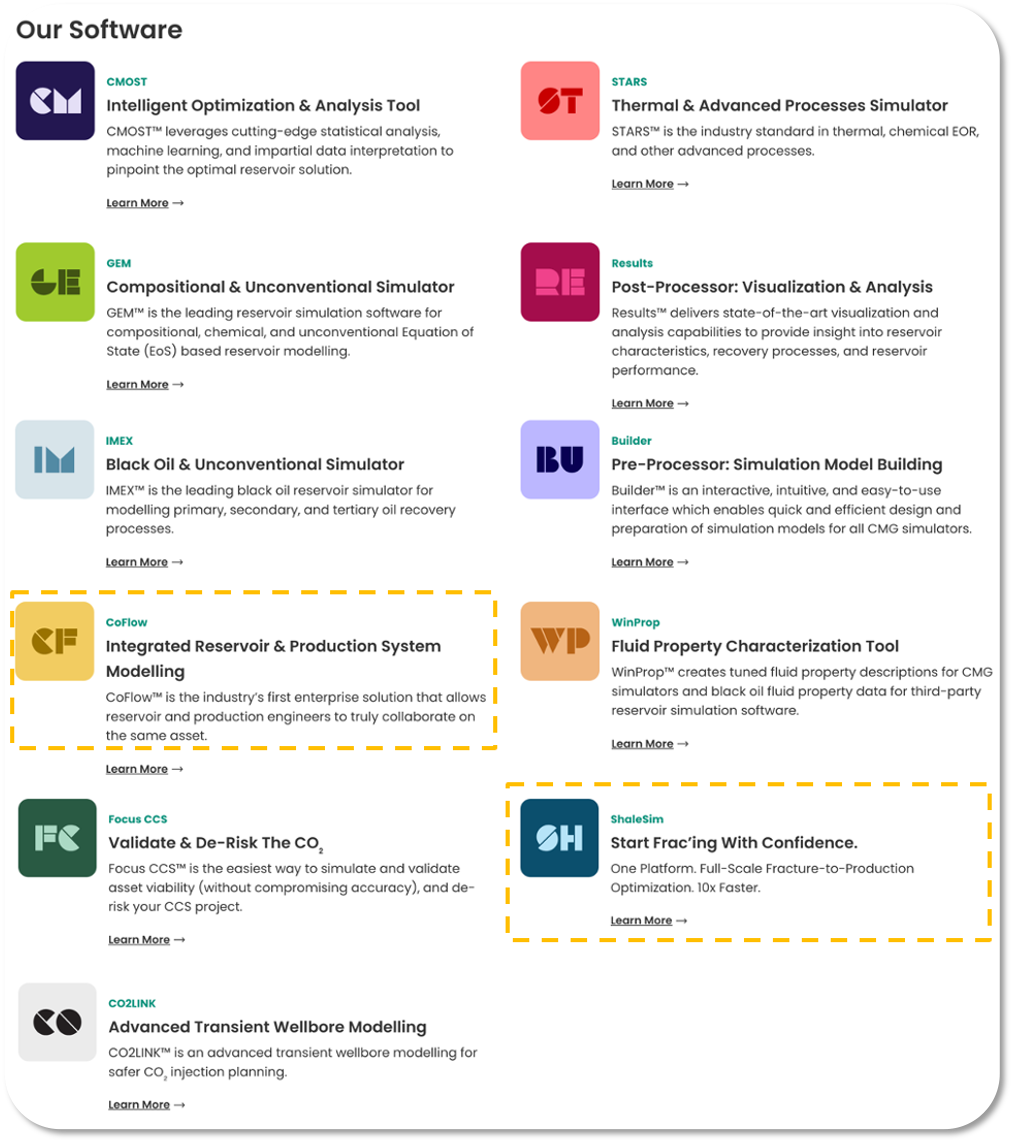

At its absolute baseline, CMG has earned itself a pretty solid moat in upstream oil and gas reservoir simulation.

When supermajors need to figure out how multi-billion-dollar thermal or chemical enhanced oil recovery (EOR) projects will behave underground over a 30-year horizon, instead of guessing, they’ll use CMG’s core physics engines (STARS, GEM, IMEX).

Once an operator populates a reservoir model with decades of historical data, ripping that software out is pretty close to a nightmare.

CMG operates on a beautiful negative working capital model. E&P clients pay for their software licenses 100% upfront on day one.

And.. they gets to hold that advance cash like an interest-free loan to fund operations before even delivering the full service.

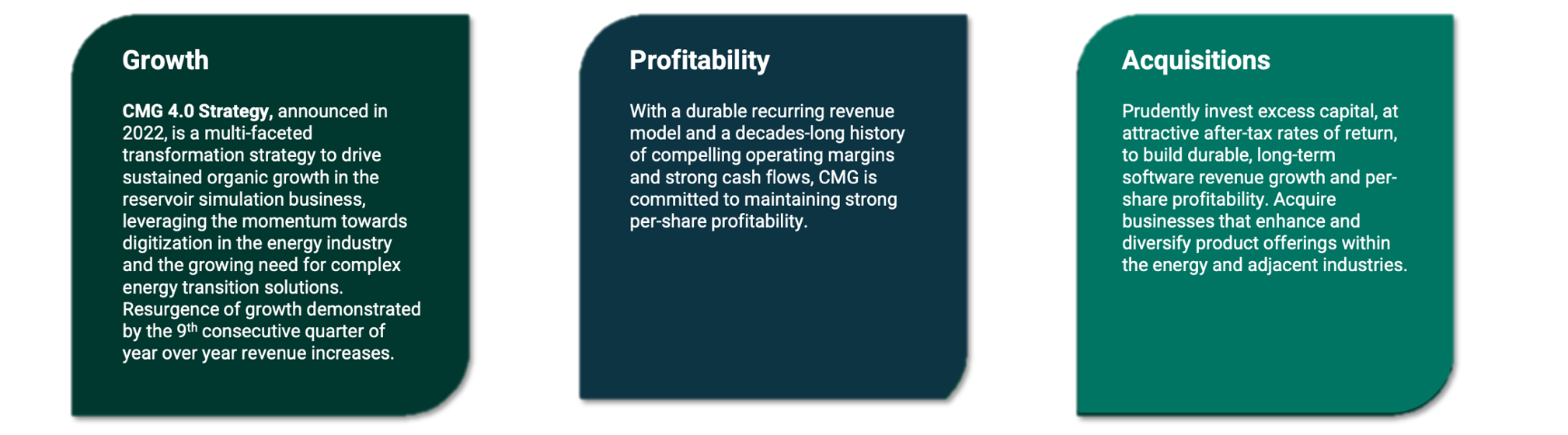

Under the new CMG 4.0 strategy, management has pivoted from a single-product footprint into a serial vertical market software (VMS) acquirer.

To fund this new playground, the CEO made the ultimate alpha move: slashing the legacy dividend by 80% and reusing cash in much more efficient ways by allocating optimally into M&A, R&D and buybacks.

They’ve stacked the board and executive team with heavy hitters straight out of the Constellation Software ($CSU) and Roper Technologies ($ROP) ecosystems to run a highly disciplined M&A playbook.

Between late 2023 and early 2026, they deployed over $90m to buy four founder-led software targets, systematically expanding their grip across the entire upstream workflow.

The following post is a hyper-detailed deep dive that has been cooking for about three months. It includes firsthand perspectives from a wide range of participants, some of whom will remain anonymous for confidentiality.

Inside, we’ve incorporated exclusive insights from 18 first-hand interviews with executives of supermajor (clients), primary competitor employees (and their feedback), and direct commentary from executive management, including but not limited to:

Pramod Jain, CEO

Kim MacEachern, (extraordinarily competent) Director of IR

As always, the bottom third of the post is dedicated to diving deep into the financials, risks, and value-unlock catalysts for this company, but here is what you should know upfront:

Top-tier leadership: Their CFO comes straight out of Constellation Software, and they are executing a phenomenal M&A playbook across the simulation software value chain.

Aggressive buybacks: They are heavily buying back their own shares.

A game-changing launch: Just a few weeks ago, they rolled out a major new software deployment targeting unconventional reservoir modeling that changes everything.

🌱 Origin Story

There’s nothing like starting with a bit of an ideological rant. We all love a good underdog story where government intervention actually creates some good.

Let’s call this The Hermit 0, Gov of Alberta 1.

CMG began in 1978 within the Chemical and Petroleum Engineering Department at the University of Calgary.

Dr. Khalid Aziz, a prominent professor and researcher, founded the organization using a research grant from the government of Alberta to build a digital simulator capable of modeling complex subsurface oil reservoirs.

For the first 19 years of its existence, CMG operated strictly as a non-profit research foundation. Its primary mandate was to solve the complex scientific challenges associated with the thick, geologically hostile heavy oil reservoirs and tar sands of Western Canada.

The inception math and fluid mechanics engines were built by top-tier scientific minds during this era, including long-term pioneers like engineer Long, who spent 47 years deep in the core physics code before his recent retirement.

As the energy landscape shifted during the 1980s and 1990s, easy-to-extract primary oil reserves began to deplete globally. Operating companies were increasingly forced to deploy secondary and tertiary enhanced oil recovery (EOR) techniques (this is important), such as thermal and chemical injections, to extend the life of their assets.

CMG, right time and right place, capitalized on this transition by introducing commercial software products in the late 1980s that could enforce complex physics across underground systems with unmatched precision.

This high-science approach turned CMG into the de facto gold standard for advanced reservoir simulation, as international operators realized that miscalculating subsurface dynamics could instantly ruin a billion-dollar asset.

Seeking the capital necessary to scale its global footprint, the organization officially transitioned into a publicly traded corporation in 1997, listing its shares on the TSX.

Throughout the late 1990s and 2000s, the company expanded its core engine into global energy markets and leveraged its thermal simulation expertise to build an early, dominant position in adjacent environmental workflows like carbon capture and storage (CCS) simulation.

Note: Carbon capture may sound like nothing, but it’s one of those technologies that’s very important, especially in a Biden-like era.

Despite decades of consistent profitability and reliable cash generation, the company historically behaved more like a publicly traded university than an aggressive software growth enterprise.

Product development frequently prioritized interesting scientific anomalies over clear commercial paths.

This operational framework shifted dramatically in 2019 when Mark Miller, a veteran enterprise software executive celebrated for his role in building Canada’s preeminent serial acquisition machine (Constellation Software), joined CMG’s Board of Directors.

Miller assumed the role of Chairman of the Board in 2022 and recognized that CMG’s deeply entrenched customers, high pricing power, and massive switching costs formed an ideal foundation for a software rollup platform.

IR: […] CMG’s history is that it was a carve out from the University of Calgary. (It) was originally a research foundation, but in many ways it was still being run as a research foundation.

So there was lots of pet projects going on, really smart people solving really hard problems, but with no commercial lens on it.

So we apply that same return lens or IRR lens on an internal initiatives as we do to M&A.

In May 2022, the board appointed Pramod Jain as Chief Executive, intending to institute “institutional” capital discipline and starting the era of what is now known as the CMG 4.0 Strategy.

Under the CMG 4.0 mandate, executive leadership pivoted the business model from a single-product footprint into an acquisition-focused software aggregator targeting specialized tools across the entire upstream energy workflow.

To fund this pipeline, Mr. Jain executed an aggressive capital allocation pivot in August 2025, slashing the company’s long-standing quarterly dividend down to a nominal token to unlock cash flows for R&D and buybacks.

This internal architecture was deepened in July 2025 with the hiring of Vipin Khullar as CFO. Khullar, who brought eight years of disciplined acquisition and shared-services experience from (Perseus) a prominent Constellation Software subsidiary, focused immediately on constructing a repeatable M&A diligence playbook.

Further strengthening this rollup governance, CMG appointed Christopher Wright, not the US minister but a thirty-five-year board veteran of the elite vertical software acquirer Roper Technologies ($ROP), to its Board of Directors on February 10, 2026.

Note: I know, that’s a lot of names and links. The jist of it is that $CSU is very embedded into the current final form of CMG (dragon ball reference right there).

These aggressive capital deployment initiatives have completely transformed the business model of company. Between late 2023 and early 2026, CMG successfully deployed over $90m to acquire four distinct software targets:

Bluware in September 2023 for cloud-native AI seismic interpretation;

Sharp Reflections in November 2024, led by CEO Bill Shea, for high-performance computing pre-stack seismic analysis;

SeisWare International in July 2025, led by CEO Murray Brack, for integrated geological mapping and 3D well design; and

Rose Subsurface Assessment in March 2026, led by Managing Partner Peter Carragher, to capture the market for probabilistic risk assessment and resource estimation.

We’ll discuss these targets thoroughly one by one in the business model segment.

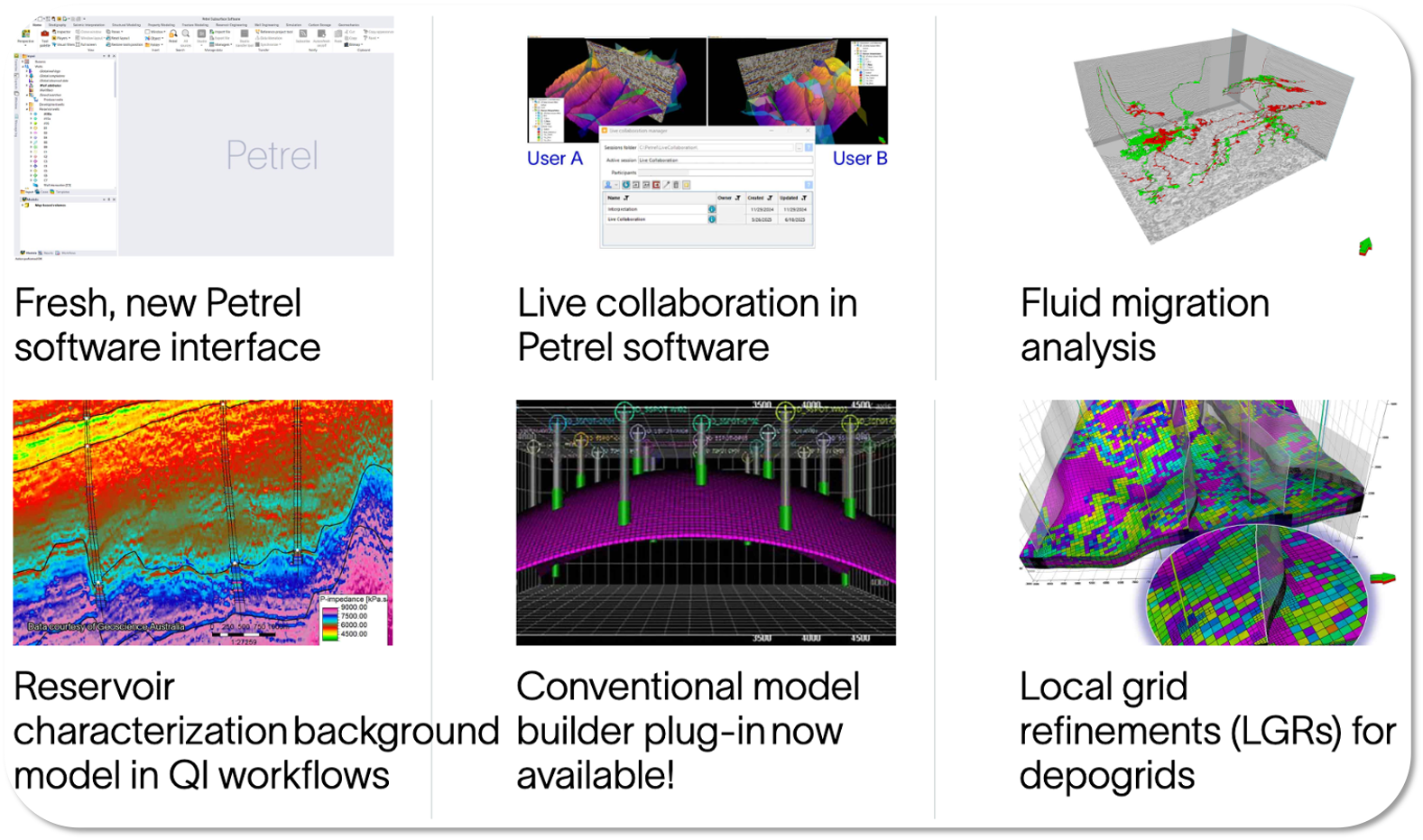

Moving on to more recent milestones, CMG has rolled out a few massive platforms, including CoFlow and their brand-new ShaleSim, which is making its official debut as we speak at the URTeC conference (yes, I scheduled this a few weeks ago).

We want to treat these products for what they really are: the future of the company. We’ll expand on them in the Business Model section.

To wrap things up, we’ll look back at a highly insightful, older presentation from the exact moment the company transitioned its core engines into the cloud.

What they uncovered during that initial migration lays the blueprint for how they are setting up to corner the market today..

🌐 Industry Overview and Competitive Landscape

We already covered the broad strokes of upstream, midstream, and downstream oil and gas in our Spartan Delta piece, but today we’re focusing on the upstream software market.

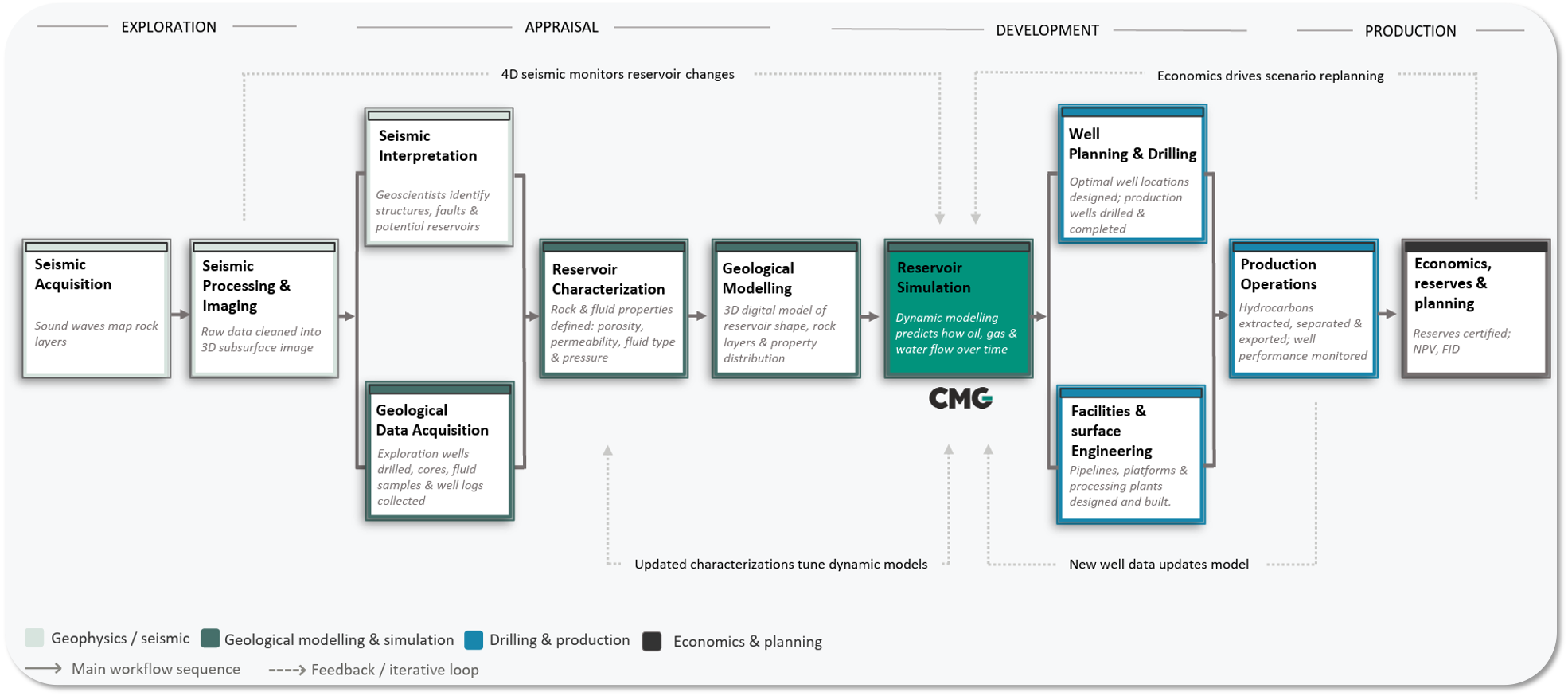

Before we jump into the specific companies, it helps to look at how the entire value chain fits together. This is a multi-billion-dollar network split into four core phases:

exploration

appraisal

field development, and

production operations

It’s an extremely interconnected ecosystem where one or two giant players dominate massive slices of the market, yet they frequently rely on smaller, specialized niche tools to actually make their workflows function.

Here’s a quick infographic summarizing each phase and the key players we’re about to break down:

Upstream Software

Phase #1: Exploration & Geophysics

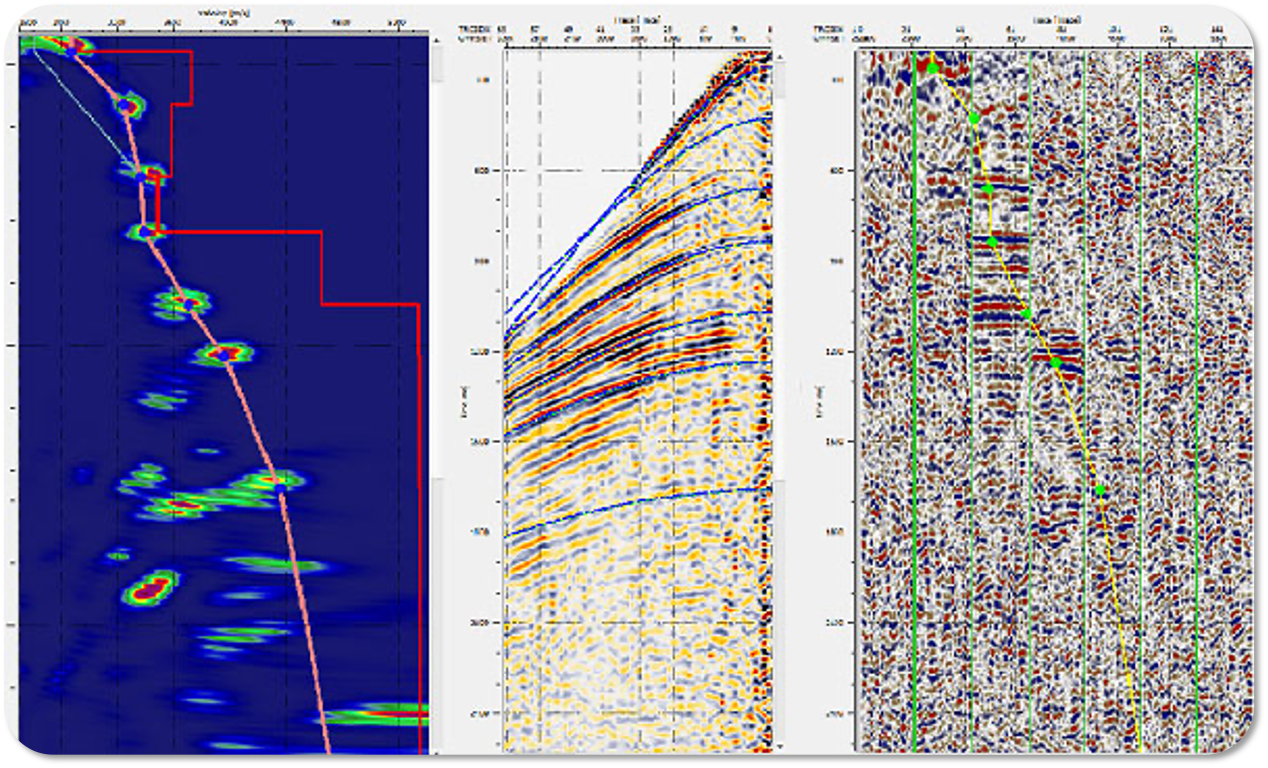

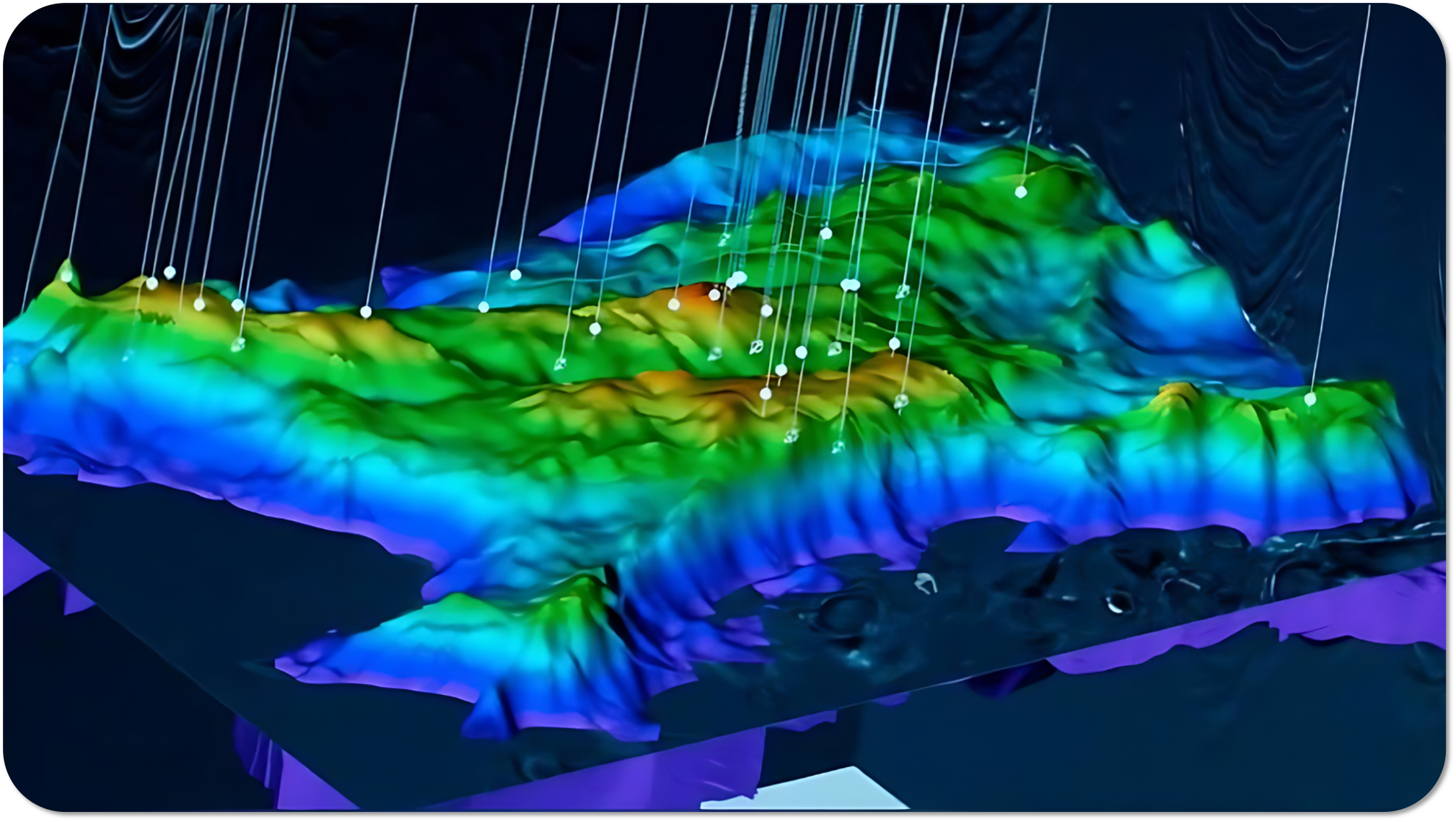

This is the land of Seismic Processing & Interpretation. Sound waves are pumped into the ground, captured as raw data, and cleaned via high-performance computing (HPC) into 3D subsurface images. Geoscientists then manually or algorithmically interpret these images to map geological faults, stratigraphy, and identify potential hydrocarbon traps.

SLB controls the undisputed lion’s share of this segment. Its flagship platform, Petrel, commands an overwhelming 90% to 95% market share inside the geosciences workflows of the world’s major oil companies and national oil corporations.

Large enterprise alternatives include Halliburton’s DecisionSpace and Emerson/Paradigm.

Small-to-mid-market operators or independent consulting shops frequently deploy lower-overhead solutions like S&P Global’s Kingdom (IHS Kingdom) or SeisWare (part of CMG*).

Note: If you want to read further about this topic, here’s a really good article explaining the topic thoroughly.

Phase #2: Appraisal & Geological Modeling

Once a prospect is discovered, engineers collect well logs, physical core samples, and fluid data to build a static 3D digital model of the reservoir’s exact shape, rock property distributions, and internal boundaries.

Because geological modeling bridges the gap between seismic interpretation and dynamic engineering, SLB (Petrel) seamlessly flows its dominant position down into this phase. Halliburton is the secondary enterprise heavyweight.

Niche specialized tools like Rose Subsurface Assessment (part of CMG*) capture a highly specialized subset of this market by layering probabilistic risk metrics and resource estimation directly over static structural datasets.

Phase #3: Field Development

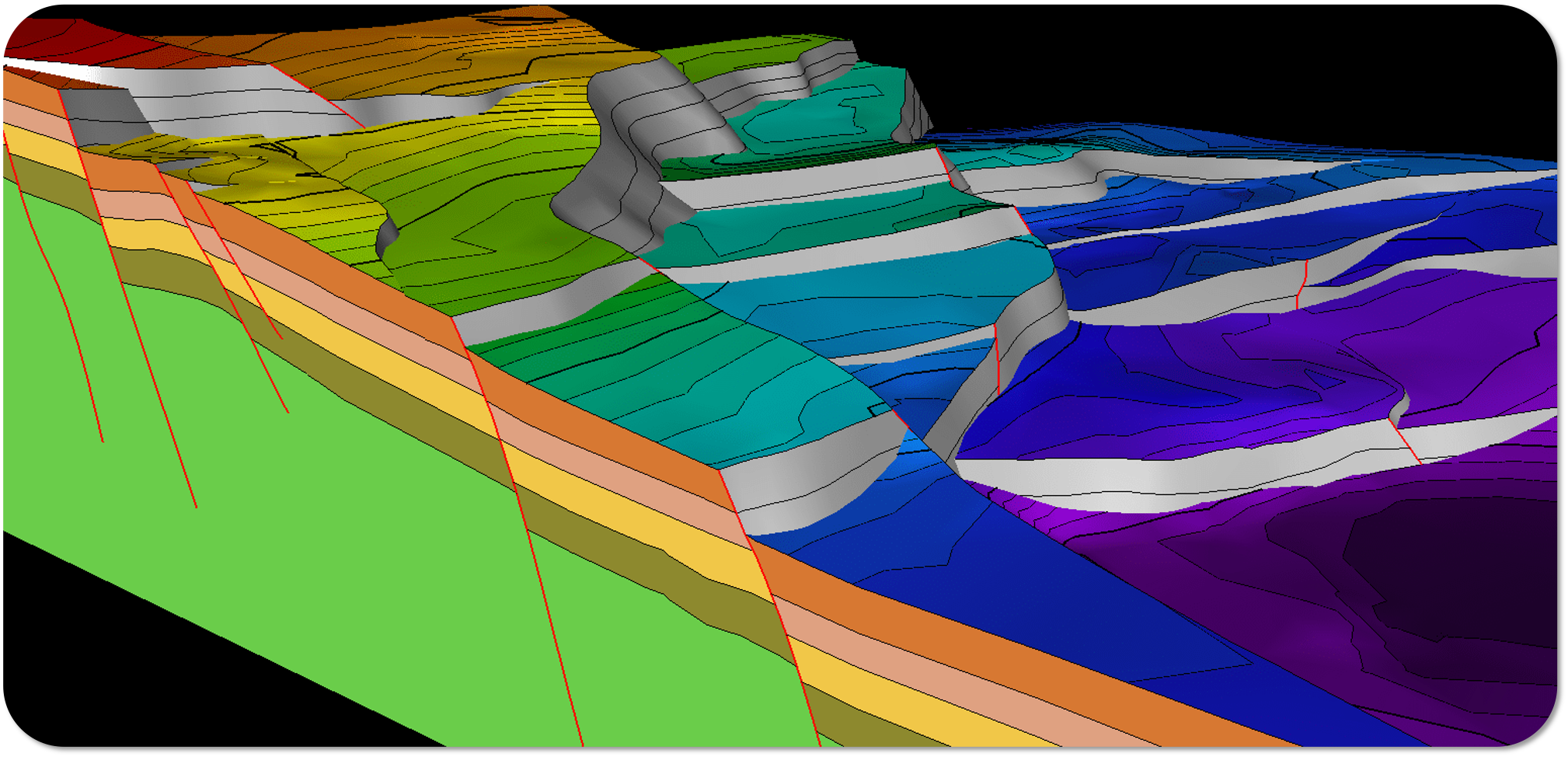

We’re now hitting close to home with Reservoir Simulation & Surface Engineering. This is the highest-stakes computational step in the chain. Dynamic reservoir software applies physics-enforced laws of thermodynamics and fluid mechanics over 15-to-50-year projection lines to simulate how oil, gas, and water will actually flow under different drilling and recovery strategies.

This is a tightly consolidated duopoly/oligopoly market. SLB (ECLIPSE and INTERSECT) and Computer Modelling Group (IMEX, GEM, STARS) own the dominant tier-1 enterprise installations globally.

SLB definitely has the horizontal reach across the board, but CMG holds the dominant market share in highly complex high-CAPEX assets.

To be very specific, CMG dominates in areas related to controlling heavy oil, thermal composition modeling (SAGD), and complex chemical Enhanced Oil Recovery (EOR) workflows.

The primary modern challenger taking market share from legacy installations is Rock Flow Dynamics’s tNavigator, which has grown aggressively in regions like Western Canada.

Phase #4: Production Operations, Reserves & Economics

Once wells are drilled, software takes over to automate trajectories, monitor active well flow rates, manage surface processing pipelines, track depletion, and dynamically certify proven reserves for corporate balance sheets and regulatory compliance filings.

Production engineering surveillance is dominated by major service providers like SLB Avocet and Baker Hughes. Again, SLB proves to have an end-to-end solution.

The final accounting, asset valuation, and macro-portfolio planning layer is highly fragmented, led by large aggregators and business software ecosystems like Enverus and Quorum Business Solutions (these guys also absorbed Aucerna, which used to be a competitor in the space).

We know it’s a bit confusing for non-technical people.

Plus, we are, after all, bombarding you with information… so here’s the industry map set up by CMG to help you better visualize the space.

Major Players

SLB (formerly Schlumberger)

We eed to dive a bit into these guys. SLB is the undisputed heavyweight of the digital oilfield.

Their core leverage starts with Petrel, which, again, commands an overwhelming 90-95% monopoly over the global static geological modeling market.

Because geoscientists build the initial 3D subsurface asset models inside this Petrel environment, SLB uses it as an immediate entry point to push its own dynamic simulation engines, ECLIPSE and INTERSECT, which historically dominate conventional reservoirs with a 60% market share.

If an engineering team wants to deploy CMG’s software instead, they are forced to deal with the severe operational friction of manually exporting and converting historical models out of the SLB ecosystem.

This conversion process is incredibly difficult, causing deep pain and aggravation for asset teams who risk losing consistency and accuracy across their predictive models.

What makes SLB an omnipresent threat is their ability to shift the commercial conversation away from grassroots technical performance toward top-down corporate packaging.

Because they handle massive physical oilfield service contracts globally, they can leverage deep corporate partnerships that a specialized software firm simply cannot match.

SLB regularly packages their software tools into broad enterprise-level licenses, pitching all-in bundles directly to procurement departments and chief financial officers. When an oil company signs a sweeping master agreement with SLB, standalone invoices for independent point-solutions suddenly look standalone invoices for independent point-solutions suddenly look redundant and inefficient to executives.

If you’re an engineer, you definitely don’t want to look stupid to your CEO.

This aggressive, top-down strategy played out directly in CMG’s recent major contract loss with a massive customer in the Middle East. On the ground, the asset teams ran a rigorous software evaluation, and CMG actually won the technical bid because its engines handled complex subsurface workflows far better than the competition.

The field engineers had been happily using CMG software for a long time and fought hard to keep it. However, SLB completely bypassed the technical users and went straight to the C-suite with an aggressive corporate pricing strategy. The decision was ultimately forced from the top down, mandating an enterprise-wide switch to SLB regardless of what the engineers on the ground preferred.

Despite these aggressive tactics, SLB’s land-grab strategy has created a natural defense mechanism for specialized players like CMG. Because operators fiercely guard their proprietary asset data and fear losing pricing leverage, most standard oil and gas companies refuse to be completely locked into a single mega-vendor like SLB.

It is standard industry practice for operators to maintain licenses with more than one simulator concurrent with SLB, using alternative engines to check model accuracy and protect themselves from vendor leverage.

Even when SLB wins a top-down corporate contract, converting highly complex models can take years with no guarantee of accuracy, leaving frustrated engineering teams actively advocating to bring CMG’s trusted math back to the field.

Rock Flow Dynamics (RFD)

RFD is a nimble, fast-growing tech firm that poses a direct structural threat to CMG’s legacy geographic dominance.

Their core product, tNavigator, is an integrated software suite built from the ground up to utilize modern GPU and High-Performance Computing (HPC) hardware architecture.

It combines geological modeling, PVT properties, and reservoir simulation (black oil, compositional, thermal) into a single user interface. RFD is applying severe competitive pressure on CMG’s core market share, particularly in mature basins like Western Canada.

Halliburton (Landmark) [NYSE:HAL]

Note: Do yourself a favor… if you haven’t seen Adam McKay’s Vice, go watch the trailer right now.

It’s highly educational, incredibly sharp, and fun as hell. Absolute masterpiece. Plus you’ll understand a lot about Halliburton.

Like SLB, Halliburton competes by wrapping software tools into its massive corporate oilfield services bundle.

The company has two core products: Nexus and VIP (Multi-component reservoir simulation software).

Nexus supports full subsurface asset asset-modeling configurations. Halliburton targets enterprise operators who prefer a single, diversified generalist vendor to handle broader asset development over standalone, specialized tools.

ResFrac

ResFrac is a highly focused niche player operating primarily in the North American shale market.

Their core product is a coupled hydraulic fracturing and reservoir simulator.

Historically, CMG’s legacy simulators struggled to model the complex, rapid physics of hydraulic fracture networks, allowing ResFrac to win market share among unconventional operators in tight shale plays.

Rather than paying an expensive valuation multiple to buy ResFrac, CMG built its own tool, ShaleSim, which officially launched to directly target and reclaim market share from ResFrac across emerging global unconventional plays like Argentina.

Stone Ridge Technology

A boutique technology vendor targeting extreme parallel computing workloads.

Their core product, ECHELON, is an ultra-fast GPGPU-based reservoir simulator built explicitly for (massive) data-heavy structural processing runs.

It targets specialized asset groups, prioritizing pure raw computation speeds for immense grid-block fields.

What They’re All Missing

Despite billions of dollars in digital oilfield investments, the upstream software stack still suffers from deep, legacy design gaps. These represent massive pain points for operators, but, more importantly, they are clear entry points for specialized tech players.

Understanding exactly where these cracks are is vital. With AI now accelerating software development, the ROIC in this space can be massive, both through organic, in-house builds and by acquiring nimble players who are reimagining how supermajors approach these problems.

CMG seems uniquely prepared for both.

But is the rest of the industry actually competitive, or are they completely asleep at the wheel?

It all comes down to the following critical structural blind spots that current players are either failing to address or ignoring...