🎙️ Raketech - Business Model Overview w/ CEO Johan Svensson and CFO Måns Svalborn

Breaking Down Raketech’s Niche Marketing Winning Formula: Business Insights from Svensson & Svalborn

My dear fellow Hermits 👋

Welcome back to 🧙♂️ The Hermit 🧙♂️

ICYMI:

🧙♂️ The Hermit Way: 2025 Predictions

🧗 Our Investing Journey: Lessons from 3 Elite Managers

💼 The Hermit Portfolio: November Update

If you haven’t yet, subscribe to get access to this post, and every new post

Interview Transcript and Commentary

On December 17th, we had the opportunity to talk with the CEO and CFO of Raketech (STO:RAKE), Johan Svensson and Måns Svalborn.

Unfortunately, the interview audio will not be published at the company's request. However, we managed to squeeze out permission to publish the transcript of our conversation alongside commentary on the most important bits and pieces.

The commentary will include some ideas pertinent to the company’s development that were not discussed during the interview.

As always, this content is intended for informational purposes only and should not be taken as investment advice. The author does not represent any third-party interest, and he may be a shareholder in the companies described in this series. Please do your own research or consult with a professional advisor before making any financial decision.

Table of contents

Business Model

Q: I divided this chat into four different sections: business model, alignment, m&a, and business developments or new developments

Let’ start with the business model. Could you describe what affiliate and sub-affiliate marketing is, what Raketech does, and what the market for sports betting and casino leads is?

Johan: Yeah. What we call Affiliation marketing, it's our own asset which we own and operate ourselves, either through employees in-house or through strategic partnerships with entrepreneurs.

These assets generate leads for casino and sportsbook operators, and we are getting paid when these leads are registering an account and making a deposit to these operators. So that's affiliation marketing where we drive the leads ourselves.

Then we have SubAffiliation, which consists of two platforms: Raketech Network and Affiliation Cloud. On these platforms, we are helping other affiliates and publishers sell their traffic to the operators and optimize their business.

Raketech Network is basically an affiliate network that connects advertisers and affiliates. It helps affiliates earn commissions by promoting online gambling and betting services.

On the other hand, Affiliation Cloud is Raketech's SaaS platform that gives affiliates all the tools they need to run their own affiliate marketing operations smoothly. It’s more of a white-label solution

As a decent-sized affiliate player, we get better commercials. So we can help them to optimize their business. For this, we take a markup of around 20. So it means if we sell the traffic to the operators for 100 euros, 80 € goes back to the lead generator the publisher (the affiliate) and we keep 20€ for offering this service

Q: How is this complemented by the other part of the business, the tips and guides, the sort of on the background?

Johan: Betting tips and subscription. We divested land-based betting tips and subscriptions earlier this year and the remaining business is fully online. What we do here is sell the betting tips, we produce content sports content to engage freelancers and editors. This attracts users to consume this content.

And if they like some extra content or betting tips around specific games, then they pay for a subscription to get access to that information. And, on these assets, we also have affiliation marketing, meaning that if we try to convert these users to a sportsbook operator scene in the U.S.

If you have bought or purchased the betting tips, you will most likely place a bet somewhere. We then try to send that player or that user to a sportsbook operator. So we have multiple revenue streams, both the subscription for the betting tips and the affiliation revenue from the sportsbook operator.

Q: Understood. You just mentioned the physical versus online space. Well, you described it as land-based. Why the full transition from a little bit of physical and mostly online to purely online?

Johan: Online is our core business. We acquired these businesses around three years ago. And back then they were making most of the leads, generating them online, but they were converting them offline from a land based office and that is not scalable in the same way.

So we have, during the year, transformed it and managed to sell our land-based business back to some of the key stakeholders in that company. Now we are fully focused on converting leads online.

Q: Understood. There is a portion of it that is strongly linked to strategic partnerships with third parties. Can you discuss a little bit what the main partnerships are, how they work, how do you guys benefit from them?

Yes, we have a couple of strategic partnerships within affiliation marketing. It means that we have teamed up with entrepreneurs with a good track record of running these assets.

So instead of having employees in-house operating these assets, we operate them together with entrepreneurs who are good with driving these type of SEO assets. For this, then we have a profit split or a revenue split. Raketech takes care of sales, invoicing, finance services, and hosting while partners in these partnerships, take care of building content, SEO strategy and product development.

We split the different working streams between us and the entrepreneurs.

Q: There seems to be a lot of localized competition, in other words, very small players, but they seem to be monopolies in the segment.

And I wanted to touch a little bit upon the sort of consolidation of the segment. Can we discuss a little bit the competitive advantage of Raketech, whether scale allows you guys to sort of retain some clients or fix some of the prices? And any differentiating factors that Raketech sort of brings to the table.

Johan: Are you talking about affiliation marketing or are you referring...

Q: Affiliation and sub-affiliation, yeah.

Johan: Okay, and local, what was your exact question?

Q: Well, there seem to be two types of players. You've got, you know, Catena Media, XL Media, Gentoo, Acroud, Better Collective, etc. These are sort of competing players that are consolidating the sectors and their strategy is buying smaller players.

And at the same time, you've got these smaller players, which are essentially people like, in your case, Cazumba would be a very good example. Where it can operate as a stand alone individual IP, or it can be part of a bigger enterprise like Raketech.

And I wanted to know the differentiating factors that you guys sort of bring to the table, like whether scale helps.

Johan: Now, Raketech, we have also been very acquisition driven over the years, meaning that we have acquired smaller players, smaller affiliates in the markets.

And this has been... We've done it, Catena Media did it, Better Collective did it, so did gambling.com. I think it's been the affiliate sector has been very acquisition driven and a lot of consolidation has happened.

What we see now is more that many of the smaller affiliates today, they are more looking to get support with the sales side, the commercials, we can help them through our SubAffiliation platform.

Instead of acquiring smaller affiliates, we are more focusing on supporting them with better commercials and different services related to the sales side of it. We haven't been active on acquisitions since three years ago since we did our last acquisition.

Affiliate marketing traffic is largely dominated by local champions who excel at targeting specific niches of players. These affiliates cultivate and sustain unique gaming subcultures, shaping unwritten rules and behaviors that create a highly sticky environment for players accustomed to their ecosystems.

In contrast, SubAffiliation operates on a volume-driven model, where the largest bundles typically deliver the lowest cost per lead for acquirers, prioritizing scale over niche engagement.

M&A Activity

Q: Understood. With regards to the actual business, there's two or three points that have to do with the alignment, but I'm going to touch upon the M&A side since we sort of dove into that.

There seems to be a massive transition, not only from you, but from the sector, from like the Nordic space into North America over the last 5 years. Can you sort of explain why North America is the current focus?

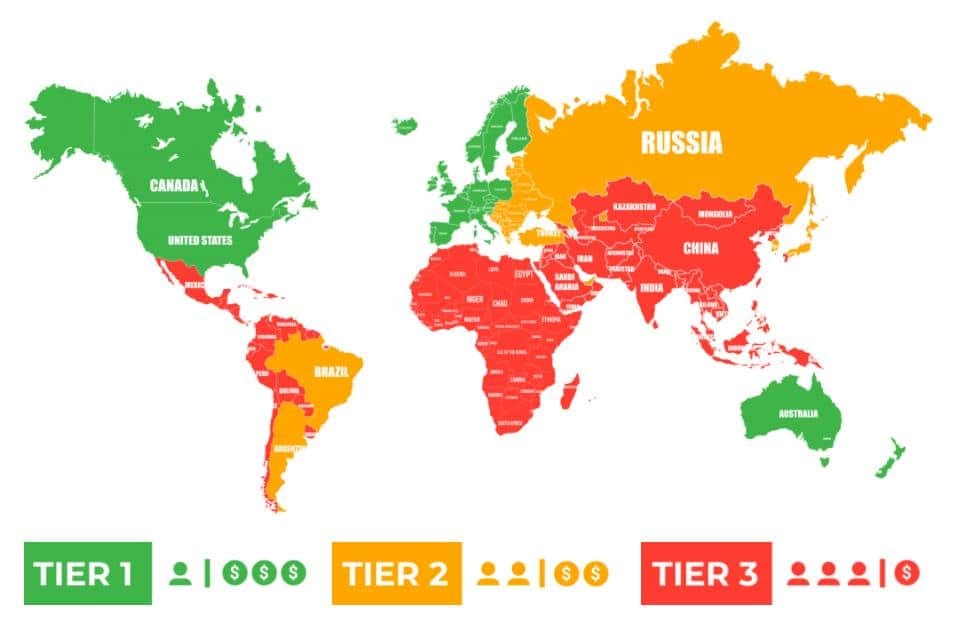

Johan: Yeah, North America and the US is estimated to become the biggest regulated market in the world. And yeah, the last... four or five years here, a big number of states have opened up for sports betting and a few of them have also regulated casinos.

So it's been a big focus for a lot of affiliate companies, including ourselves. It has shifted a bit recently for some of us. We've been struggling with running U.S. in a profitable way.

It's more expensive with local U.S. resources compared to, for example, Europe. We're focusing on the U.S., especially through SubAffiliation where we, during Q3, managed to secure a partnership with a Tier One Sportsbook operator to help them with tier two and tier three affiliate operations.

Basically, if you were a smaller publisher or an affiliate, you had to go through our platform Affiliation Cloud to get to deal with this operator. So US is a focus for us through tips and subscription business, which is almost 100% US, but also through SubAffiliation.

The Tier system is a measurement of payment per lead generally based on geographical location. Factors like local competition and regulation also affect this division.

For Raketech this can be particularly powerful as core competitors are focusing on tier 1 U.S. Affiliation, while Raketech is focusing on becoming the portal of choice for tier 2 and tier 3 Affiliation while remaining the tier 1 SubAffiliation leader.

Q: Understood. On the M&A front, I would very much like to touch a little bit upon the Casumba deal, if that would be possible, and the sort of valuation side of things.

Johan: I think it's too early to draw any final conclusion on the Casumba acquisition. We acquired it in Jul 2019 with a very low upfront payment and more of an earn-out component. The business had a very successful 2022-2023, which made the earn-out payment increase significantly.

And this year we ,together with the founders are still on board, we haven't been able to perform as well as we did last year, which have had a big impact on our affiliation marketing revenue. But we are still comfortable in the strategy we have to turn these assets around.

So I think it's still too early to evaluate this acquisition. But it's clear that this year has been a big disappointment in terms of Casumba performance. But we remain confident in our strategy.

Casumba is a Japanese intellectual property acquired by Raketech in 2019 for €2.0 million (3x EBITDA). The acquisition included an earnout component, which could be settled in both cash and shares.

While we won't delve into the specifics of the deal, it's important to note that it featured a five-year structure that concluded in July 2024, with no cap on the earnout payments. As a result, Raketech now faces a required payment of €9.9 million by July 2025, along with an additional €20.6 million payable by September 2026. Ironically, these same assets have been among the most impacted by recent changes to Google’s algorithms.

Q: How are you looking at this M&A strategy in the near future? Will you keep on purchasing companies between three and five times? What are you looking for? Are you focusing more on the support of current IP?

Johan: Right, M&A is not something we focus a lot on. We're focusing on our operations and turning our business area into organic growth again. We have the liabilities to pay to Casumba founders, which has led to streamlined costs this year, we had 18% lower costs YoY in Q3.

So we are in the middle of a transformation when it comes to our operations, which also includes more types of strategic partnerships. We communicated a new partnership in Q3 for the slot portfolio where we have teamed up with founders. So right now, I would say that M&A is not the main focus for us.

In the future, I would say M&A could be of interest, but it needs to add a lot of strategic value. Building organic is what we focus on at the moment.

Shareholder and Management Alignment

Q: Understood. On the alignment side of things, I would very much like to know about your transition. I know Johan, you've been the CEO before of the company, but it would be very useful to understand Oskar's exit and how you guys sort of reshuffled management on that front.

Månz, you were also a part of the team with Oskar. I would love to get your take on the new leadership. You know, talk bad about your boss for a second. I'm kidding, I'm kidding.

Johan: Yeah, yeah, I'm one of the founders and CEO up until summer 2017 when I stepped down to focus more on the commercial side and M&A. Then I left the management team 2019 and worked full time from the board with different strategic projects.

And then I rejoined in August 2022 as COO before the board decided to let Oskar go in January this year (2024). I was appointed as interim CEO and then as permanent from May this year.

I haven't sold a sharing Raketech in eight years and have no plans to do so. I'm very committed to this company. What I think is important is to always find the best possible way to operate our portfolio of assets.

If it means to do it with our headquarters in Malta, or if it is through strategic partnerships or strategic deals within SubAffiliation with that needs to be decided case by case. The most important is to have a streamlined core team who knows our business very well, who can open up for good recruitments or for strategic partnerships in some way.

Regarding Oskar, I prefer not to comment on his strategy, but Oskar was a good contributor to our growth during his four years as CEO for the company.

Q: Understood. Would you care, Månz, to comment on the different leadership strategies from Oskar versus Johan?

Måns: Thanks for putting me on the spot hahahaha 😂

I think I can give you a general comment. So I think a company goes through different phases. There's a need for different leaders in these different phases.

I think an Oskar came in five years ago Raketech focused a lot on acquisitions. Oskar had more of an engineer personality. So he helped out a lot with structuring the organization and the business and so forth, which I think made sense at that point in time.

Now with Johan coming in, there's a lot more commercial focus, which I think makes sense now at this point in time where we have a nice portfolio of assets. We have the SubAffiliation part of it and the US part of it, but I think we're getting a really good commercial push out of Johan's leadership.

Q: Beautiful. That also links to a question I discussed a few months ago with Edvin. And that was your role, Johan, versus the role of the other co-founder, who's Eric Skarp, excuse my poor pronunciation.

Combined, you two, you own like 15 or 16% of the company, and you do have this dual dynamic, if I'm not mistaken. Can you comment on that?

For context, as of Q3 2024, the ownership split included Johan Svensson (7.73%) and Erik Skarp (7.85%)

Johan: Yeah, the relation between me and Eric?

Q: Well, if you want to talk about the relationship, that would be fine, but it's more to do with how you deal with Raketech and the day-to-day problems versus like the larger scheme, what does Raketech look like in five years type question.

Johan: Okay. Eric is the CEO of our B2C/B2B business, which was part of the group. But then we decided in 2016 to divest Raketech, when we needed the biggest need for new capital, which also led to the IPO.

So I think it's important now given the situation Raketech is in. We need to start generating shareholder value for our shareholders.

We are trading at an all-time low since we got listed. There is not a lot of confidence in the share price or from investors. And I think it's really because we have liabilities. How I see it is, if we can continue with delivering good cash flow over the next two, then we will be able to pay down earn out payments and we will have a very nice company with producing a good portion of cash flow.

That is how I see it as a shareholder in Raketech and as CEO, it is my objective to deliver on this plan. Which will mean that we need to focus on which what will have an impact for the long term.

So we've done a lot of changes this year and we will continue to assess and evaluate portfolio of assets to make sure that we have the best possible foundation for long term organic growth.

[…]

Q: With that in mind, and going back to the questions and alignment, and giving back to the shareholders, with you guys owning a fair chunk of it, Dividends and Dilution.

Those are the two questions: What are you planning on doing with dilution and the really, really high dividend that you used to have, which is no longer the case? Because as you mentioned, you guys need to pay like 10 million bucks now and 20 million in like the next two years.

Johan: Yeah, sure. I cannot answer the question for the board, but I can speak as a shareholder. I would prefer not to get diluted on on these levels. Definitely not.

We have liabilities to pay down or refinance in some way. To get the balance sheet healthier is definitely what we are focusing on.

Q: Okay, I'm guessing dividends will probably be on the table after like 2026 once everything is done, but right now you guys aren't even thinking about it.

Johan: It's a question about capital allocation. We paid dividends in 2023. I think it comes back to delivering shareholder value and dividend is one component, as we pay out the profits or part of them.

The company has pursued an ambitious M&A agenda, entirely driven by its exceptionally strong free cash flow (FCF) performance. While there is some dilution tied to earn-out agreements, the capital structure has remained largely unaffected, with minimal changes to both debt and equity.

The Casuma deal, however, introduces significant financial commitments, This significantly hampers the company’s capacity for inorganic growth, although it does not constrain organic expansion given the high ROCE in existing IP.

Additionally, Raketech has a history of paying dividends, achieving dividend yields of 7-8% in previous years. To provide context, if the company were to allocate a similar proportion of its free cash flow (18%) for 2024, with an expected FCF of €17 million, this would equate to €3.22 million in dividends. Based on the current market capitalization of €17.31 million (198 million SEK), this translates to an impressive dividend yield of 18.6%.

Recent Business Developments

Q: Understood. I mean, your free cash flows are super, super healthy and overall the company seems to be very healthy, but as you mentioned, the earn-out payments will weigh heavily in the short term.

There is one thing that is technically financial as well, which is the impairment, which I would love to talk about.

Google algorithm and asset impairment. How reversible do you guys see this and whether, adapting to the new standards, sort of allowing the Google Bard/Gemini to get trained? Is that an option? What are you thinking about the whole topic?

Måns: Sorry, you had a term there that I didn't pick up on. Which one?

Q: I was talking about the asset impairment, which is essentially your IP from the Google term changes. Google seems to be very focused on training its AI models. And obviously companies that don't want to share their data are sort of placed at the end of the lists. What are your thoughts on this and how are you sort of counteracting this? Is the impairment sort of “reversible”? Do you think your IP is still good?

Johan: In the end, if we lose ranking and that means the decrease in revenue, that could of course have an effect on the balance sheet.

Måns: Yeah, unless the question was related to the balance sheet, or is it the actual performance of our assets in relation to an updated...

Q: It technically is related to the balance sheet. I sort of wanted to wiggle my way into it, but it's more about addressing the changes.

Måns: Yeah, that's one part of it, definitely. Then it's other parts as well, so you can weigh in changes in regulatory state, for example, in different markets and how they relate to the specific assets that could trigger a change in the valuation of the assets, for example.

Even tax regime changes in a market could change the valuation of the assets, for example. So it's a bunch of indicators, a bunch of triggers that could have an effect on it.

If it's reversible or not. Well, technically you can't reverse it, but it's all of these factors you need to weigh in if it's whatever change, if it's sustainable or long-term, if we perceive it as long-term or not.

Q: Do you perceive it as long-term in that case? The changes in the Google algorithm.

Johan: Well, Google updates their algorithm constantly, and then you have bigger Google updates, which are now. So now we're starting a new Google update they announce. They call them Google core update when it's a significant one.

What's in it for us is to adapt. We have to make sure that our content and that our products are relevant for Google to favor them ahead of our competitors. And that's something I've been doing for the last 15 years and something we as a company we are constantly improving.

This year we got a big hit on the Casumba assets and which has been our reported numbers as well. But for an entrepreneur like me working with SEO, that is a part of the game.

We started this company to build a poker platform 15 years ago. We were ranking very high on Raketech. Now poker is not a big thing anymore. Raketech was banking on the trend of online poker. When it decreased significantly, we started to focus on casino and sports betting assets instead

That's something Raketech will continue to do and we have to adapt and make sure that we are competitive enough. It could take some time sometimes to recover and we can't guarantee that we will recover and get back to the same result before.

At the same time, in some other markets during the year, we have actually managed to increase our positions and gain traffic. But we took a big hit definitely this year with our Casumba assets, which we are working very hard to recover from.

Q: The commercial refocusing makes a lot of sense now that you sort of frame it in that way. It'd be very interesting to know whether that SEO optimization, which you have been doing for quite a long time, whether that's all in-house or whether you outsource part of it, whether you get help from some strategic partners, whether it depends on like a country to country level.

Johan: It's a mix. To be competitive, you need to have the right expertise and you need to make sure that you have the right execution.

And some assets fit better to sit in-house with employees here at the office. And some of them sit better with entrepreneurs, which in a strategic partnership.

So it's about evaluating asset per asset to make sure you have the right skill set and execution power to deliver. So yeah, that's something we constantly evaluating.

But what's been this year, we've managed to launch one more strategic partnership. We can either choose to close down the team in house or give them other priorities, other assets to work on and team up with entrepreneurs, which we did with our Slot Java portfolio, including the Spanish assets SlotJava.es.

Q: I wish I was recording this because when I mentioned SEO optimization, your eyes, they brightened up.

Johan: hahaha 😂😂😂

Vision for Raketech

Q: With that in mind, I think that's super, super useful information. And I do have one sort of last closing question. And that's where is Raketech in 10 years?

Johan: In 10 years… Raketech will be the leading SubAffiliation platform in the industry where operators and publishers are connecting to benefit on our commercial network and great services.

That could open up for investment. We can own some of these assets that are connected to the platform. But it could also be that we don't have any ownership of these assets. So it's a mix. But what all assets will benefit on is our commercial network of connections and deals, which we have been building up for the last 15 years.

Q: Can you touch a little bit on that actually? Ownership versus non-ownership of these assets. Why would you own them or why would you not own them?

Johan: Yeah, today we take one of our assets, CasinoFeber in Sweden. It's connected to Affiliation Cloud. We own it 100%. Then we have another asset in Sweden, let's say CasinoWings. It's another asset. It's owned by Traffic Labs(), but they're using our platforms to get access to good deals.

So when an account manager here for Sweden speaks with an operator, it can say, we have these five assets in Sweden where you can buy a traffic car.

It's CasinoFeber, CasinoWings, and these other assets. That operator, it doesn't matter if Raketech owns the site or if it's a partner on Affiliation Cloud. Yeah, we will still what we will do is to bundle the traffic and send it to to the operator.

That type of services, especially more regulated, matured market is something I think will will explode. And we have a little bit of a first mover advantage. We managed to close this this partnership with this US operator. And this is something we will focus a lot on next year to close more more of these exclusive partnerships.

Q: Understood. That's a brilliant answer.

That was extremely helpful. I took a lot of notes and I will be writing a really, really bad report on you guys because that's the... No, I'm kidding. I'm kidding. 😂 Obviously, this was extremely useful. I think you guys are brilliant and I wish you all the best of luck.

And if I can help you in any shape, way or form, I am more than happy to provide my support free of any charge. I am a shareholder, as I told you.

Johan: Great, great. As I said, I will be in Barcelona, arriving […], leaving […]. If you'd like to meet up, happy to set some time aside. If not, we can speak in connection with Q4.

Q: Beautiful. I'm not very interested in Q4, I am very interested in 2027 Raketech. That's what I'm very interested in.

Johan: Great, great. Okay, have a good festive season and let us know if you need anything.

Q: You too. Merry Christmas and thank you very much. Special thanks to Edvin (IR).

Thanks for the post! Interesting business.

I did seo amazon affiliate sites and some heavily seo dependent ecommerce sites for a number of years. The platform risk for me with relying on google algorithms is too much. I had industry leading brands in niche spaces which ended up dumpster fires with one algo tweak from google. It’s part of the industry and you can adapt but it’s gut wrenching revenue volatility.

I’m very intrigued as to why they didn’t want the interview posted 🧐